SoFi 2Q23 was almost flawless

Wow. That was a better quarter than I honestly thought was possible. There are some things I’ll need the 10-Q to update, but I am extremely pleased with the quarter that SoFi just put together. I think most people have seen the headline numbers so I’ll just highlight some things that really stuck out to me and that haven’t been covered quite as thoroughly or are less obvious (except for talking about member growth – everyone has already talked about but it’s so good that I have to talk about it too).

Members

This was the first quarter I finally gave in and accepted that members would be less than 500k. For the past year I’ve continued to think that at some point the fact that the total membership was so large that the member adds above 500k/qtr again like it did in 4Q21. But after 5 straight quarters, I finally decided that SoFi was just curtailing ad spend to hit the 400k number because of the focus on profitability.

Boy was I wrong. The previous high water mark for members added in a quarter was 523k in 4Q21, but they blew that away by adding 584k in 2Q23, a 10.3% QoQ increase. Not only that, but sales & marketing spend only increased from $175M in 1Q23 to $183M in 2Q23, a QoQ increase of just 4.4%. The customer acquisition cost, which had been ticking up, dropped to its lowest level since 4Q21.

I personally am a big fan of this kind of hyperscaling. I’d rather they push profitability out if it means they are getting more new members at lower prices than their historical average. More members than ever at a lower CAC than they’ve had in the past year is a great thing. Getting people in the ecosystem is absolutely vital for the long term business, which is what I care about most, so this is great news. Doing it at better than expected cost is just the chocolate sauce, whipped cream, and cherry on top.

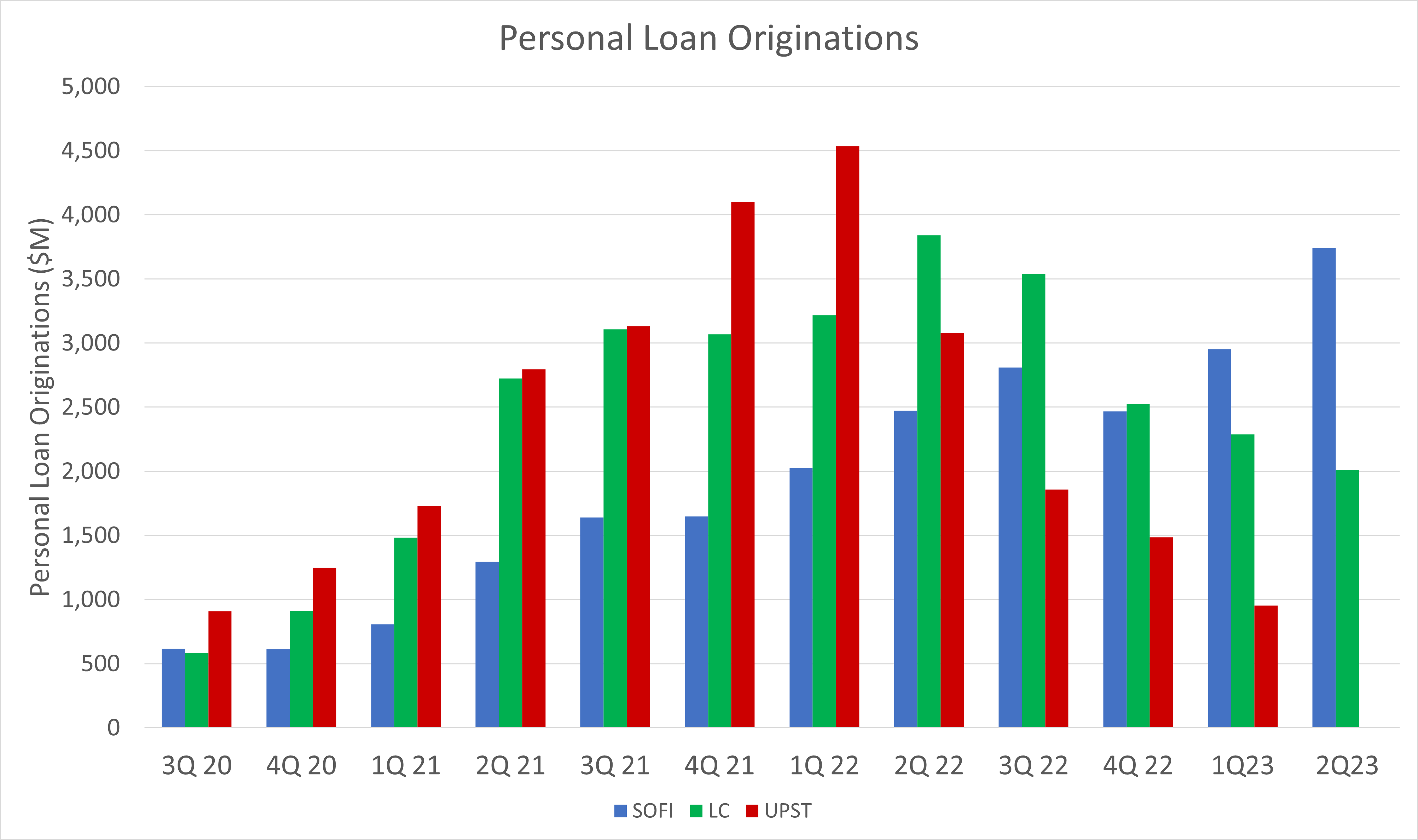

Personal Loan Originations

Following the theme from above, this number came in way above my expectations. SoFi is taking significant market share from their competitors. Check out the graph of quarterly originations for the three biggest fintech personal loan lenders SoFi, LendingClub, and Upstart.

And here is one with QoQ growth rate. Upstart (who reports next week) has been shrinking for four straight quarters as has LendingClub. I expect Upstart originations to tick up this quarter, but they have a very long way to go to get back anywhere near their high point. This is actually the highest QoQ growth SoFi has seen since 2Q21, and the base they are growing from is so much larger now.

The most exciting part is that defaults on their personal loans are down QoQ. That’s incredible and not what LendingClub or Upstart are seeing. SoFi’s underwriting continues to outperform while their market share increases.

At some point they are going to have to start selling more loans if they want to continue to grow personal loan originations. That’s a topic I’ll have to cover once the 10-Q is out because I really need capital ratio numbers and need to know how many loans were held to maturity to address it properly. Something for readers to look forward to.

Galileo

The tech platform bounced back and set a new ATH for revenue in the quarter, though only just. This was a very welcome sign, but there is still a lot of work to do here. They guided for this to be flat in 3Q before growing again in 4Q23. That would be fine with me, but I really want to also see margins expand. They seem to be bottoming out, but they need to make progress toward their stated goal of 30%+ margins because their contribution margins have been hovering just under 20% for the last three quarters. We are supposed to start to seeing the infrastructure investments like moving to the cloud pay off this year, and that’s where it should show up.

This remains the one part of the business where execution has not been as good as I would have liked for the past year. We need to see accelerating growth combined with margin expansion for me to feel good here, although we won’t really be able to see that it’s a true trend until probably a year from now. Given the incredible execution everywhere else in the business, the headwinds in the macro, and the pivot to larger and more established clients, I’m willing to give them time for this story play out. I’m also confident it’s a big focus for them internally as well.

SBC

This is the only real negative from the earnings. I saw this coming but just didn’t have time to get out an article about it in the last quarter. SoFi granted a ton of RSUs last quarter, 27.5M of them to be exact, which is the most they’ve ever given in a quarter. That also isn’t entirely surprising because the first quarter always has the highest number of granted RSUs. The expensing of the PSUs is ending this year, but the new RSUs are so large that they are offsetting that drop. Chris Lapointe also commented that this number will be up modestly in the 3Q and 4Q in the earnings call:

As we move toward expected GAAP net income profitability in the fourth quarter, we expect stock-based compensation and depreciation and amortization expenses to be slightly higher than reported Q2 levels in both the third quarter and fourth quarter of the year.

SBC both in absolute and relative terms had been trending down nicely. This quarter’s print reversed both of those trends. About a year ago they said they want to be in single digits of SBC as a percentage of revenue by 1Q24. That, unfortunately for investors, is not going to happen. It means they’d need to be doing $750M+ in revenue by 1Q24, and that’s just not going to happen. Investors need to keep an eye on this moving forward because dilution can eat away at gains and increasing SBC will be a drag on GAAP earnings.

That’s it for today, as always there will be more to come in the future. Thanks for reading everyone. Please make sure to become a free subscriber by entering your email, or a paid subscriber if you feel so inclined. Always 100% voluntary.

Disclosures: I have a long position in SOFI.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Great article. Great quarter. Re SBC - I think it makes sense that they would issue a bunch of stock with the shares beaten down over the last two years. Most of the previous SBC is underwater and won't pay off for employees although still has to be expensed. So reloading the employees for the next leg up makes sense and is fairly standard for tech companies.

Thank you for the article, Chris.