SoFi Fair Values Part 2: Insights from the 10-Q

At the end of my recent post about fair values, I said I’d post more info after doing a review of the 10-Q. This should be taken with the context that was provided in that article. I realize the narrative around SoFi has moved on, but I invest on fundamentals, and this topic is absolutely going to come up again so I’m going to try to help investors understand it better.

Alright, onto the fun stuff. Let’s discuss the fair values and what the assumptions are to calculate them and whether they are, well, fair. The fair values are determined mainly from three inputs: prepayments, defaults, and the discount rate.

Prepayment rate: If people pay their loans off early, it results in less interest income for the people who would be buying them, so a lower prepayment rate leads to higher values.

Default rate: This one is pretty obvious, but if defaults increase, whoever owns the loan not only doesn’t get any more interest, but also has to take a huge loss on the unpaid principal remaining. This is probably the biggest weighted factor in the fair values

Discount rate: The technical definition of a discount rate is the interest rate used to calculate the present value of future cash flows. People who used discounted cash flow models to arrive at fair values of stocks are very familiar with this concept. An easy way to think about this for me is the opportunity cost of my capital. If I can get a risk-free 5% short-term bond, I’m not going to invest in a personal loan that is only yielding 6% because of the risk of default. Typically, the riskier the asset, the higher the discount rate because people want to make sure they are compensated for the risk.

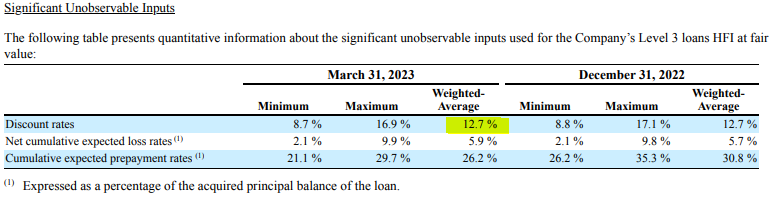

Let’s look at what SoFi used for these three parameters in the most recent quarter:

Let’s focus on personal loans because those make up the majority of the loan book and that’s where the biggest controversy has been. Prepayment rate is what it is and nobody really worries about it. Let’s discuss the other two numbers. Annual default rate averages to 4.6%. Current annual default rates are actually just under 3%, so this number has a fairly large margin of safety built into it.

My biggest concern with the fair values

The discount rate is a bit of a red flag to me. A 5.5% discount rate for personal loans that do carry risk seems very low considering that on March 31, you could buy a 1-year T-Bill that would pay you 4.64% interest with no risk at all. Furthermore, this discount rate is significantly lower than competitors who also use fair value accounting. LendingClub sells almost all of its HFS loans during the period in which they are originated (they originated $1.205B in 1Q23 and only $110M of it was still on their balance sheet on March 31), but they do provide fair value estimates for the small amount they do have. Likewise, Upstart reports their loans using HFS accounting. For 1Q23, LendingClub used a discount rate of 12.7% and Upstart used a discount rate of 11.78%. Here is LendingClub’s disclosure:

Here is Upstart’s:

LendingClub’s discount rate looks extremely conservative. Upstart’s ought to be higher than SoFi’s given their loss rates are almost quadruple SoFi’s. But comparing SoFi’s number to these highlights the discrepancy. I like to call it like I see it, and SoFi’s low discount rate looks like it was given with rose-colored glasses on. This is especially true given that the discount rate should roughly parallel movements in the 2-year treasury yield and 5-year treasury yield, since those are basically the risk-free alternatives to buying personal loans. The graph below shows that the gap between SoFi’s assumed discount rate and these treasury yields has narrowed significantly during this rate hike cycle. If SoFi’s fair values are inflated, the low discount rate would be the culprit. However, I am really not qualified to be able to say what should or shouldn’t be used.

Three independent verifications

Ok, so this is where I think the bear narrative falls apart. Others have started questioning why SoFi uses a third party to establish their fair values, saying this points to the fact that SoFi may have fallen afoul of regulators and is being forced to do so. I think that’s ridiculous. Fair value calculations make up a huge portion of their quarterly numbers, and ensuring that the numbers are accurate by having a third party calculate them to remove any conflicts of interest seems like a prudent decision.

Furthermore, there is no way this is because regulators found some irregularity and are submitting them to further scrutiny. How do I know this? Because this is the exact same thing they’ve done for all their public filings. The 2021 10-K makes it explicitly clear that they were already using a third party at that point, before they had their bank charter, to independently verify the fair value calculations.

SoFi does their own fair value calculations in house. They also have a third party independently perform the exact same calculations to verify them. To me, that provides a level of safety, but it doesn’t stop there. SoFi’s yearly financial statements are audited by Deloitte, one of the Big Four accounting firms. Here is what Deloitte said about the fair value measurements in the 10-K:

We identified loans held for sale, at fair value, as a critical audit matter because of the unobservable inputs management uses to estimate fair value. This required a high degree of auditor judgment and an increased extent of effort, including the need to involve our fair value specialists.

How the Critical Audit Matter Was Addressed in the Audit Our audit procedures related to the fair value measurement of loans held for sale included the following, among others:

We tested the effectiveness of internal controls over the fair value of loans held for sale, including management’s controls over the evaluation of the reasonableness of unobservable inputs used in the valuation.

We evaluated the valuation models and the related assumptions, including significant unobservable inputs, and underlying loan data used by management and their third-party valuation expert.

We tested the completeness and accuracy of the source information derived from the Company’s loan data, which is used in the valuation model.

With the assistance of our fair value specialists, we developed independent fair value estimates and compared our estimates to the Company’s estimates.

In other words, SoFi’s fair market values are calculated monthly and quarterly by SoFi internally, at least quarterly by an independent third party, and yearly by Deloitte who do their own independent fair value estimates with their own in-house fair value specialists. I repeat again that I am not qualified to truly judge what should be used as a discount rate. However, I find it extremely unlike that not one, not two, but three independent accounting teams are all committing fraud simultaneously. This seems especially true when two of those three companies have no skin in the game and in fact would be legally at risk of being sued for hundreds of millions of dollars or more if someone can prove calculations are not in good faith. I’m not qualified to make these calculations. These guys are and they signed their names to SEC documents stating that they approve the fair values.

Fair values are lower than what their ABS would suggest

SoFi had a personal loan ABS offering in 1Q23 and also one in 4Q22. Those securitizations inform how much demand there is for their loans. The 10-Q had this to say:

For personal loans, our discount rate assumption in the first quarter reflected the lower benchmark rate and narrower spreads indicated by asset-backed security and secondary bond markets compared to the fourth quarter, but assumed a wider implied spread than our current period securitized deal and our most recent whole loan sale.

Wider implied spreads would translate to a higher discount rate than what they would have used if they had based it on the actual 1Q23 securitization. In other words, they are marking their loans to a lower value than what they should be based on the actual securitization they did in the quarter. They are marking them more in line with the 4Q22 securitization, which had tighter spreads. In other words, they are actually marking the loans conservatively relative to the in-period demand that they saw.

Conclusion

Is understanding fair values important to SoFi investors? Yes. Is there higher ROE from holding the loans than selling them? Yes. Do I still think they should have sold some loans during 1Q23 to justify the marks? Yes. Do I believe that the marks are justified at the levels they are at right now? I’m an engineer, not an accountant, and I am predisposed to believing those who are experts in the field rather than trusting my own judgement. SoFi has those experts, their third-party valuation firm has those experts, and Deloitte has those experts. All three of those groups independently have certified that these fair value measurements are accurate and I have no reason to doubt them.

There is still a lot to dig through from last earnings that I’ll be writing about. I’ll be giving updates on SBC, the tech platform, and company fundamentals. I also hope to cover some other tickers if I find the time, which is always the hard part.

Remember to Subscribe

Please make sure to become a free subscriber by entering your email. I do this analysis because I want to make sure that I am doing due diligence on my own holdings and because I enjoy writing. Taking that and turning it into in-depth articles and making visuals and graphs adds a lot of time and effort to that endeavor. I plan on always publishing everything I do for free. If you feel like my analysis has helped you, I ask that you consider becoming a paid subscriber. It isn’t too expensive, it’s only $5/month or $50/year. Always 100% voluntary. Thanks for reading everyone.

Disclosure: I have a beneficial long position in the shares of SOFI, LC, and UPST either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I have no business relationship with any company whose stock is mentioned in this article.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Hey, great blog. I’m trying to make my own analytics, but forward P/E is hard for me to predict. How you like to calculate/predict forward P/E for SoFi?