SoFi's Revenue will Soar in 2024

I’m back. Sorry, December was absolutely nuts, but my huge report is finally turned in, so my 70+ hour work weeks are done and I should get back to a normal cadence of articles (meaning at least 2 per month). I lost a few paid subscribers through the lull, but hopefully I can provide enough value to bring some back.

I recently had the opportunity to get on a call with Chris Lapointe and ask him several questions about SoFi’s business and numbers. Some of the insights I gained from that discussion will be the focus of a number of articles moving forward, this is the first of those. I’ll also try to keep articles shorter and more frequent whenever possible.

One of the questions I asked was about his quote from the recent investor conference where he said “In 2024, we expect 50% of our revenue to be from tech platform and financial services and then the remaining 50% from lending.” I thought perhaps they were talking about by the end of 2024, so I asked if that was talking about full year 2024 or by Q4 2024. He said that it’s for full year 2024. I knew that was bullish from doing some basic math, but even I didn’t understand the full ramifications of what that means until I did this analysis. I have never been more bullish for 2024 than I am now. Let’s dive in.

First, let’s give a little bit of context. From that same conference, here is the quote:

So back to your question on the growth outlook for student loans and personal loans. What I would say there is there's a lot of macro uncertainty out there right now. We're really optimistic about everything we've been able to achieve, but we also have to be mindful of what's happening around us. […] We may be in an environment that's uncertain, and we may be in an environment where interest rates stay higher and more volatile for a longer period of time. We do think that demand for our products and our ability to capture that demand will remain extremely robust, but we need to be mindful of the turmoil that's happening around us.

In that type of environment, we're going to take a more cautious and conservative approach to our lending. In that environment, our personal loans could be flat to slightly up. Our student loan business could grow just modestly, but we're going to be mindful of everything that's happening around us.

The 50-50 revenue split presupposes flat or slightly increasing revenue in lending. This mirrors Anthony Noto’s comments in the 3Q23 earnings call when he said, “think about SLR [student loan refinance] and PL [personal loans] being additive to growth, not the driver of growth as we go into ‘24.”

Bearish Case

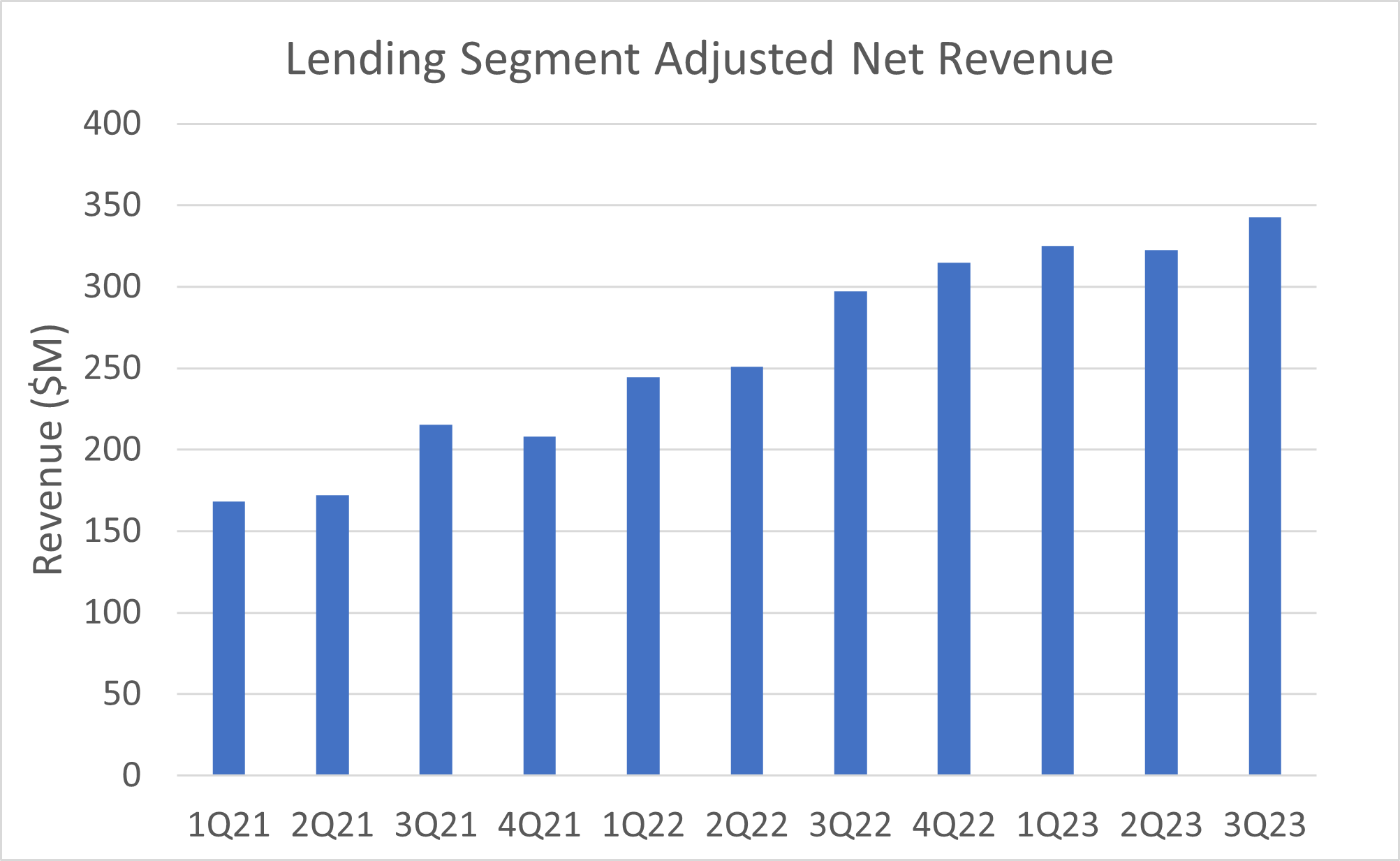

Ok. So let’s break this down into a few scenarios. The first is a bearish case that assumes no growth at all for lending. Here is lending revenue over the past few years:

In 3Q23, SoFi did $342M in adjusted net revenue in the lending segment. Let’s assume that revenue stays completely flat at that level for 4Q23 and all of 2024. This would be surprising since they still are growing the loan book substantially for at least one more quarter and they will be able to continue to add at least $600M/qtr to the balance sheet in 2024 as tangible book value grows. Assuming flat growth means that they have to pull back on originations due to capital constraints and a lack of liquidity in capital markets.

Flat revenue through the next five quarters means $1.37B in revenue from the lending segment in FY2024. This is the higher for longer scenario that they were thinking about in November when Chris Lapointe gave the comments above. If that only represents half of SoFi’s revenue in 2024, that leads to 2024 total revenue of $2.74B. The midpoint of their 2023 guidance is $2.055B, so that’s 33% revenue growth in 2024 assuming lending is flat from last quarter. What are analyst expectations?

Analysts are only expecting 23% revenue growth next year and total revenue of $2.52B. Even the bearish case would blow those numbers completely out of the water. Wall Street, once again, just does not trust what management says despite the fact that they have time and again proven true to their word. This is with no growth whatsoever, not “additive growth” or “modest growth” as Noto and Lapointe said they’d have.

Baseline Case

Lending growth for the last year as they’ve been dealing with the rate hike cycle (a headwind that is finally gone starting in 4Q23) has averaged 3.7% QoQ. Conservatively, let’s assume this same growth rate for 4Q23 (which I think is an underestimate), and then a very conservative 5% annualized growth rate throughout 2024 (which works out to just over 1% quarterly growth rate for 2024). That seems in line with the lending outlook above. That would give a FY24 lending revenue of $1.46B. If you assume the same 50-50 revenue split, that means $2.93B in 2024 revenue, or a 42.5% YoY revenue growth rate. I think this is probably around what SoFi was expecting internally in November when Chris Lapointe made the comments above. That’s nearly double Wall Street’s 2024 revenue growth estimates for 2024 if you just take what SoFi management is saying at face value.

What kind of growth could be expected for Financial Services and Tech Platform?

Ok, so what does this mean for the growth rate of the FS and TP segments? We don’t have 4Q23 numbers yet, obviously, but I project FY23 FS revenue at $436M and TP revenue at $350M. That means that combined they would make $786M for FY23. Even if you assume the bearish case is true, they need to combine for $1.37B in revenue. That means they need an extra $582M in revenue split between the two segments compared to this year. FS has a built in advantage because deposit growth gives them a very easily achievable growth vector, but TP will also need to see real growth for them to meet this guidance.

Segment Growth Rate

The last three quarters FS has grown at 25%, 21%, and 21%, respectively. 20% quarterly growth rates are unsustainable long term, but let’s assume somehow they keep that up all next year. This would probably mean they really start scaling their credit card business in addition to the natural deposit growth. That would put them at $892M of FS revenue in 2024, a 105% YoY growth rate.

That would leave $478M in FY 2024 revenue for the tech platform. That would mean 36.7% YoY growth for the tech platform. Again, this is assuming phenomenal growth in financial services and the bearish case. If you assume the same growth rate for FS and the baseline scenario above, that means that the TP needs to achieve $568M in revenue in 2024 to make up the difference and achieve $1.46B in combined FS and TP revenue next year. That’d be a 62.4% YoY growth rate for the TP next year.

Can you imagine how the stock would rerate if by the end of 2024 the following scenario happens?

Five straight quarters of GAAP profitability

Accelerating revenue growth of 40%+ YoY

Capital-light, high-margin technology platform growth is 40%+, allowing it to get a hybrid tech multiple (and even a 36.7% YoY growth rate is excellent)

That is effectively what management is guiding for with the 50-50 revenue split. Is 40%+ revenue growth in the TP really achievable? Let me pull a couple of quotes from the earnings call, investor conference, and shareholder Q&A:

Chris Lapointe:

We are nearing a growth inflection point in our tech platform segment and demand for our combined product suite from large attractive players is the highest that we've ever seen.

You're going to see an acceleration of revenue in our Tech Platform business as a result of the change in strategy to focus on more durable, larger financial institutions and larger customers with large installed bases. We've never been more excited about the demand that we see in the Tech Platform business. We're in conversations with a number of the top financial institutions right now in RFPs, and couldn't be more excited about the revenue opportunity there.

Anthony Noto:

The demand from traditional financial institutions and new categories is the most robust that we've seen. While the lead times for winning RFPs and ensuing integrations are long, measured in many quarters, not months, their transition to modern processing and modern cores is playing out in real time the way we envisioned it would. […]

We launched a corporate credit solution, which is designed to modernize expense management for both financial and non-financial corporations by introducing a central account with a single credit limit. In addition, we've expanded our Buy Now Pay Later offering to allow lenders to offer it as a form of working capital loans for the small business clients, a great example of the joint Galileo and Technisys capabilities. […]

From a geographic perspective, we received MasterCard certification to provide our payment cards and processing services and five new LatAm countries. Additionally, we have continue to see great product update and new stand-alone products such as our payments risk platform product, which has recently been launched to the entire financial services ecosystem not just existing Galileo clients, as well as Konecta, our natural language AI-driven intelligent digital assistant, which provides faster resolution of customer contacts and reduced contacts per customer for our partners as well as SoFi.

The results of our strategic switch are really paying dividends. And right now, we're in RFP status with a number of large financial institutions. We've actually won a regional bank deal, that's one component of a larger piece of their business that will come on over the next 18 months to 24 months. But the pipeline is very strong in both financial institutions, incumbent banks and non-financial institutions as well as B2B. And so, the growth prospects that we're expecting there really started to come through in a much bigger way as many institutions are under pressure to upgrade their technology and to go after new growth opportunities.

Given those comments, and the fact that they have continually reiterated the 50-50 revenue split next year highlighted above, the TP looks poised for that inflection point that Chris Lapointe spoke of. Also, because these contracts take quarters to finalize, it seems like management should have excellent line of site on future revenue growth. The math by itself leaves almost no room for interpretation. Either management is lying, or the 50-50 revenue split is what they truly foresee. If the 50-50 split is true, the tech platform growth is going to reaccelerate and SoFi will begin to demand a greater tech multiple.

I don’t believe the 50-50 split will happen (Bullish Case)

I don’t think that they’ll actually achieve the 50-50 split in 2024. However, the reason for that is because I don’t think that lending growth will be flat. I have been saying since September (and maybe earlier), that inflation was old news and rate cuts are coming in 2024. The market finally started to buy into this narrative last month. As long as the economy holds up, and I think the numbers suggest it is probable that it will, rate cuts will ease capital markets and the lending segment will see growth in 2024, especially the student loan refinance business.

I think the lending segment will grow revenue by at least 20% if the macro holds up and rate cuts come. That means that the 50-50 split won’t be achieved but only because lending will turn out better than the “higher for longer” scenario management guided for. If the lending segment revenue does in fact grow at 20% on top of the financial services and technology platform growth outlined above, a $3B year is well within reach. That would be a 50% revenue growth rate for FY2024.

Conclusion

Not many people realize how big of a deal that one sentence from management is. It seems like “we expect 50% of our revenue to be from tech platform and financial services and then the remaining 50% from lending” is such a simple statement, but the implications are incredible. Those implications include:

Financial services is poised for another 100%+ year of growth

The technology platform will grow at 40%+ next year

If there is any growth in lending at all, it will be a blowout year

2024 is shaping up to be a very fun year for SoFi investors. Remember to subscribe if you haven’t already. Lots more analysis incoming. If you want to hear more from me, consider becoming a paid subscriber because the more I make the easier it is to justify the time spent on making investing content. One of my new year’s resolutions is to start a YouTube channel this year. I need ~100 paid subscribers to justify that time and I’m at around 60 right now.

Subscriber update

Thank you to everyone who has become a paid subscriber. I am back down to 60% of my Tier 2 goal. I plan on ramping my content output as paid subscribers increase. Here are the content tiers:

Tier 1 – About 2 articles/month on the Substack. This is the level I’m comfortable at for now with what I’m making.

Tier 2 – I’ll start a YouTube channel and do at least one video every other week.

Tier 3 – A minimum of 4 articles/month on the Substack

Tier 4 – Add a weekly Twitter Spaces where I can engage better with followers and answer questions people may have.

Disclosures: I have long positions in SOFI and LC.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Thank you so very much for your concise

Report! I always look forward to reading them!

Proud to be one of your paid members Chris. These break-downs, along with your posts on X, always educate me and help block out the noise- which in turn gives me a stronger stomach to stay long as Noto & Lapointe continue to deliver to their shareholders.