Understanding SoFi's Long-term Debt

I’m still working on my article about the convertible notes and debt buyback deal. In the meantime, I still want to push out useful analysis. Debt is another part of SoFi’s business that is often misunderstood. This article should demystify why SoFi appears to have such high debt.

Also remember that this analysis is based on the most recent quarter, and with the recent deal, things are going to change. Where applicable, I’ll try to make this analysis take the new notes into account. I might put out a quick article after next earnings to give an update on the numbers presented here, because they will change. The analysis and methodology, however, will not change.

Debt

One important thing to remember is that SoFi is a financial institution. If you are used to looking at balance sheets from software and technology companies, you need to recalibrate the way you analyze the data. Banks operate with a different paradigm, and everything about their assets, liabilities, and cash flows needs to be understood with proper context.

Peter Lynch is one of my investing role models. He once said "It is very hard to go bankrupt if you don’t have any debt." One of the things I look for in an investment is a company with low debt, so you might be surprised to see that SoFi has a lot of debt on its balance sheet and it is by far my largest position. For a company with a market cap of ~$7B at the time of writing, $5.2B in debt sure seems like a lot. Let’s dive in and I’ll show you why I’m not particularly worried about it.

Cost-of-business debt

For a bank, loans are an asset since they make money on the charged interest. Deposits and debt are a liability since they pay interest on them. As of 4Q23, SoFi has $23.0B in loan assets measured at fair value (see above). Those loans are backed by three separate buckets: deposits, warehouse facilities, and SoFi's own capital. Deposits cost SoFi 0.5% APY if they are in a checking account, 4.6% APY if they are in a savings account as of the time of writing, and some CDs out as well. The average of interest they paid across all their deposits in Q4 was 4.31%. Their average cost for warehouse facilities in Q4 was 6.59%. So warehouse facilities cost them 2.28% more than their deposits. Warehouse facilities are therefore a necessary evil until they have enough deposits to cover all their loans.

SoFi also packages up some of their loans into securitizations. You’ll notice that the warehouse facilities and securitizations both appear on the liability side of their balance sheet and for accounting purposes, they are counted as long-term debt.

Here is where the disconnect happens. Every dollar of warehouse facilities and securitization liability has a corresponding asset that is worth more than the debt. Additionally, as soon as loans are sold or paid off and removed from the balance sheet, the “debt” is immediately paid. That's why I call this cost-of-business debt, it is all backed by a tangible asset that they are making money from. This isn’t “debt” in the standard sense of something that the business is going to get a bill from in a few years down the road. It’s debt that is only there because they are making profits on it right now. This cost-of-business debt totals $3.66B, which was 70% of their long term debt as of Q4.

Actual Debt

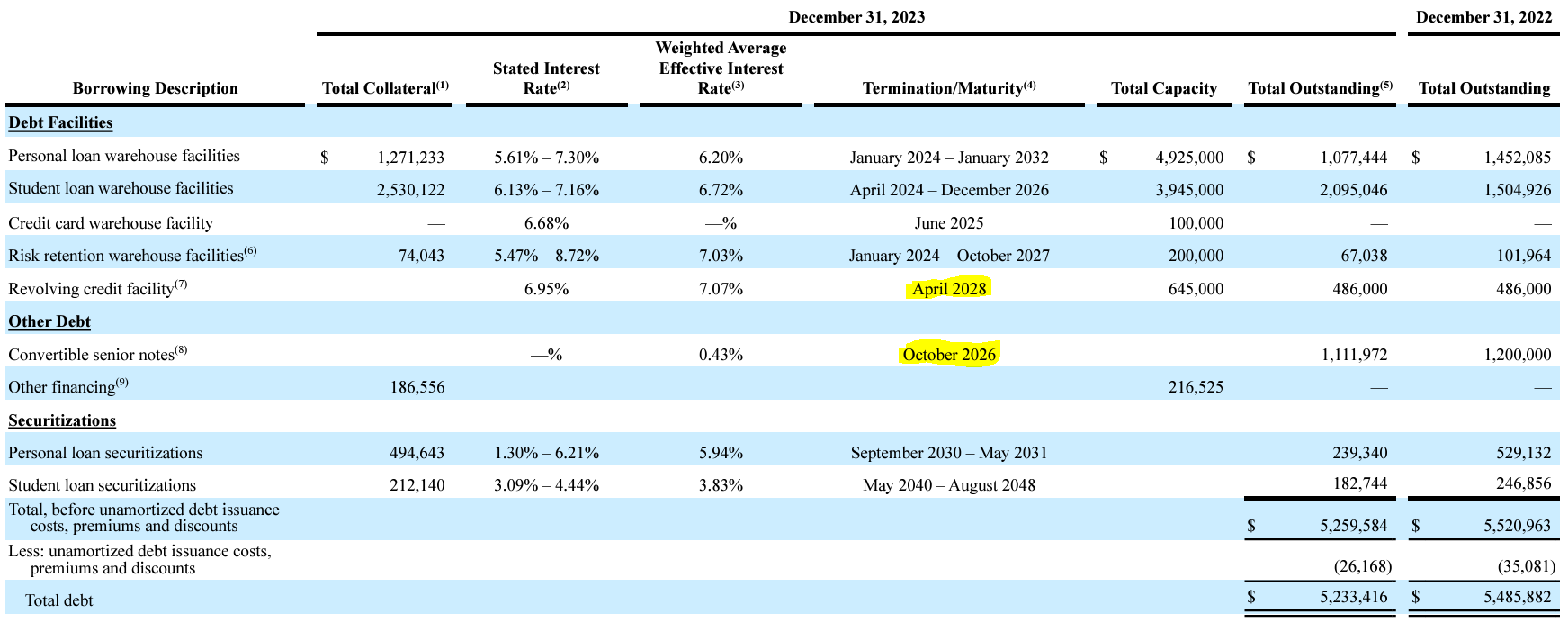

SoFi's actual long-term debt comes in two forms, a revolving credit facility and convertible senior notes. According to the most recent 10-K, here is the breakdown on what that debt costs and when it is due.

The revolving credit facility has a variable rate debt, costs them 7.07% interest right now, is drawn to full at $486M, and expires an 2028. To help clarify which convertible notes I’m referring to, I’ll refer to them by their maturity date (either 2026 for the ones you see described above, or 2029 for the recently issued ones). The $1.11B in 2026 senior convertible notes have a 0.43% interest rate until they come due in October 2026. $600M of those notes were just paid back, leaving around $512M remaining. The new $845M in 2029 convertible notes they just issued have a nominal interest rate of 1.25% and will be due in March 2029. So that means, in order of when the debt comes due, they now have:

$511M due in October 2026

$486M due in April 2028

$845M due in March 2029

Recent comments about using the convertible notes made by CFO Chris Lapointe also lead me to believe there is a decent probability some of the new cash raised by the 2029 convertibles will go towards paying off the revolving credit facility. You’ll notice that is the highest cost debt they had last quarter, even including the warehouse facilities. That means the total real long term debt for the company is not $5.23B as many who are just looking at the numbers believe. At the end of Q4, it was $1.6B, and at the end of Q1 2024, it should be no more than $1.84B. It will be less than that if they pay down some of the revolving credit facility. It is very possible that they will actually exit Q1 with less actual debt than they entered it.

Looking Forward

Optimistically, it would be great if SoFi stock goes above the 2026 convertible note conversion price of $22.41 by October 2026 so that they just convert and be done with it. If that does not happen, I sincerely hope that they have a plan in place to pay back the remaining $511M with cash instead of shares. That is probably wishful thinking on my part.

I do not expect SoFi to require any more debt moving forward as they are now GAAP profitable. Furthermore, they are growing the deposit base at a faster rate than the loan book, which means that each subsequent quarter the amount of cost-of-business debt that they require is decreasing. As they decrease the speed of the balance sheet growth this year, it is within the realm of possibility that they do not require any of the warehouse facilities by the end of 2024, although I expect it to actually happen sometime in 2025. Regardless, the balance sheet will have the appearance of lower debt as the warehouse facilities become an ever-smaller portion of their loan funding sources.

SoFi’s debt is lower than a cursory glance would have you believe. The debt that they will have to pay back has very manageable interest rates, terms, and they are not hitting any debt maturity walls. So if you hear something about their high debt, you probably don’t have to worry about it. SoFi is cash flow positive, they are GAAP profitable, and they are not at risk of defaulting any time soon.

Subscriber update

I continue to make steady progress toward the YouTube channel goal of 100 paid subscribers..

Right now I am comfortable with taking the time to write about 2 articles every month. Once I get to 100 paid subscribers, I’ll start a YouTube channel and do at least one video every other week (I plan on also posting those on X).

Paid subscribers also get access to a private X chat. If you are a paid subscriber and not in the chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

Disclosures: I have long positions in SoFi.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Thanks Chris , great info as always 🇬🇧

Every one of your article makes me a better investor. Thank you so much Chris. Happy Easter.