What Drives SoFi's growth?

I’d like to address two bear arguments that continue to resurface in regard to SoFi:

SoFi’s growth is only from excess capital and the ability to build their balance sheet

Their loan portfolio values are inflated.

Today I’ll tackle the first one. The second one, which will continue to be a matter of contention no matter how thoroughly it is discussed, but I’ll save that for a future article. Let’s dissect the argument and determine why SoFi has grown.

Is SoFi’s growth solely attributed to excess capital?

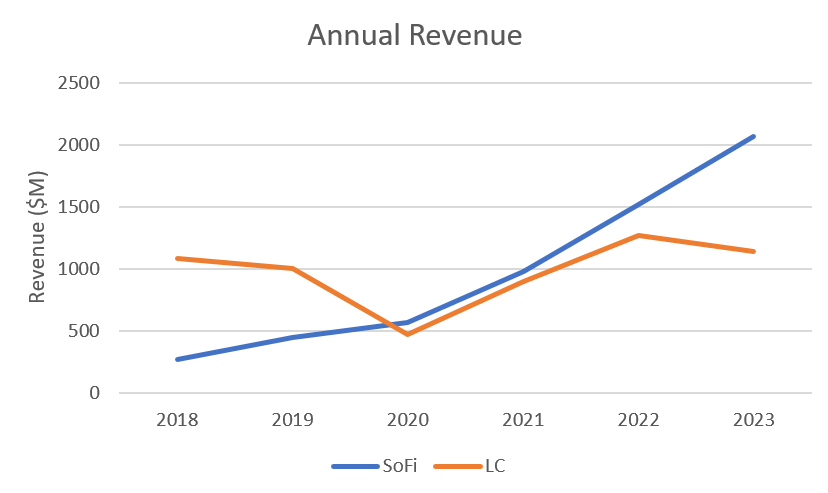

Here is SoFi’s YoY revenue growth since 2018:

2019: 87.5%

2020: 37.6%

2021: 62.6%

2022: 52.5%

2023: 36.1%

That is 5 solid years of growth above 40%, and a 50.3% revenue CAGR over the past 5 years. That is solid and consistent growth, and the fasting growing years were prior to 2022. That’s a key argument because SoFi didn't receive the bank charter until January 2022, meaning they had no excess capital to deploy prior to 2022.

The narrative that their growth is only fueled by growing their loan portfolio ignores three years of growth prior to becoming a bank. It is only in the last two years that they’ve had excess capital to deploy. They also had their biggest and most profitable business (student loans) stripped from them in 2020 and it is only now finally returning. They grew through that too. By the end of 2023 they will have more than 7.5x the revenue they had in 2018.

Also, if excess capital was all you needed for growth, then any company who gets excess capital should see massive growth, right? If only there was a company who was a competitor of SoFi and who received their bank charter in the same time period and could make for a good comparison. Fortunately, LendingClub fits all of those criteria. They received their charter in December 2021 and operate as a neobank in the personal loan space. LendingClub had a revenue CAGR of 1% over the same 5 years (2018-2023). If excess capital is all you need, they would easily have seen at least some growth. They didn’t. They saw revenue fluctuations around the pandemic, but excess capital did nothing for their overall growth story.

If the argument were true that excess capital is what fuels growth, SoFi wouldn’t have grown before they had excess capital, and LendingClub would have grown because they did. Neither of those things are true. The only logical explanation is that excess capital does not fuel growth.

What Does Fuel Growth?

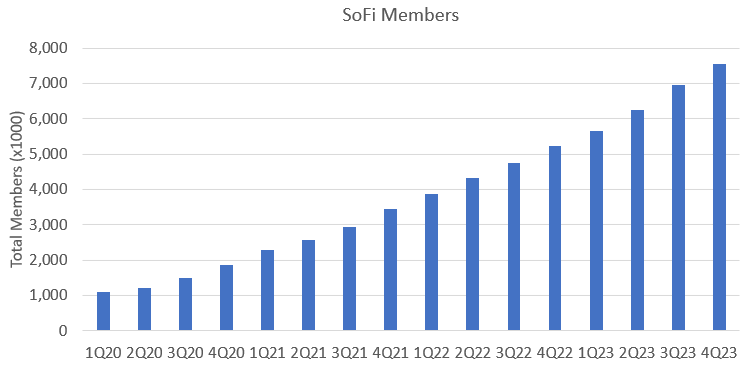

Member growth

Excess capital is how SoFi chose to grow through the past two years, but it isn't the main growth driver. In actuality, their main growth driver is product adoption and ongoing rapid member growth. SoFi attracts new high-quality members in droves. 50% of those that sign up move their direct deposit over within 30 days. That makes a sticky relationship. They monetize those customers as best they can in whatever macro environment they find themselves in, and revenue grows.

SoFi’s member growth is stead and consistent. They have only ever had two quarters where their QoQ growth rate was under 10%. That means their yearly member growth rate is always north of 40%. If they grow their member base by 40%, does it seem reasonable that they can also grow revenue by approximately 40%? Does it seem reasonable to assume that they can grow originations 40% per year? Is excess capital the reason they grow originations, or is it member growth?

Quarterly originations/member has been relatively flat as the membership has grown from just over 1M members to just over 7M members. As originations grow, SoFi ends up generating more net interest income, which has been helped by holding more loans on their balance sheet, and more noninterest income. The noninterest income comes from gain on sale. The more originations they have, the less amortization hurts their noninterest income as they are able to cycle the balance sheet faster. That would lead to continued revenue growth even without any excess capital available. This does assume that they can find willing buyers for their loans, which is a bigger question in a high rate environment. More on this below.

New members don’t only contribute to financial services growth. A key reason for their lending growth is not only the fact that they are holding loans for longer, it's also that they are growing their pool of borrowers. Many have argued that the reason they've been able to grow originations is that they have room on the balance sheet. However, that's only one part of the equation. Just as important is that they are constantly adding and monetizing new members. You don't go from $1.3B originations to $3.7B in originations while tightening lending standards without significantly growing the pool of borrowers. Member growth matters a lot. I think it matters much more than excess capital.

Member retention

While member growth is certainly great, if new members don’t stay with the platform, then they won’t contribute much to future revenue. Critics have also accused SoFi of padding their numbers because of their interpretation of what they refer to as a Member. Their definition, taken from the most recent investor presentation, is as follows:

We define a member as someone who has a lending relationship with us through origination and/or ongoing servicing, opened a financial services account, linked an external account to our platform, or signed up for our credit score monitoring service. […]We adjust our total number of members in the event a member is removed in accordance with our terms of service. This could occur for a variety of reasons—including fraud or pursuant to certain legal processes—and, as our terms of service evolve together with our business practices, product offerings and applicable regulations, our grounds for removing members from our total member count could change.

Many take issue with the fact that somebody who signed up to check their credit score once can be counted as a member basically forever. I don’t really care about that. What I care more about is whether they are churning their old members and whether they are monetizing new clients at the same rate.

To verify if churn and monetization are a problem, let’s look briefly at two data sets. The first is the originations per member graph above. It would show deterioration if there were significant churn. It does not. If originations are scaling with members, it means that both older and newer members alike are taking out loans at roughly the same rate.

Second, let’s look at financial services and lending revenue per member. This is essentially SoFi’s average revenue per user (ARPU). It excludes the technology platform since that is B2B, not B2C.

There is a slight downtrend here. That is neither unexpected nor concerning to me. There will always be some churn in the user base. It is inevitable. As you grow tot member count, the number of total accounts contributing $0 in revenue will grow over time. If you fit a trendline to the data, the average decrease is about $0.71 in ARPU per quarter. That’s about a 4% YoY decrease in ARPU. However, as established above, they are growing members at a clip >40% YoY. Churn is very small relative to growth.

Growth in 2024

SoFi is still affected by the macro environment. When the balance sheet is full, as it is now, then they need to access capital markets to sell their loans in order to continue to grow originations. This explains the acceleration in loans sold in Q4 2023. They sold more personal loans than they have in two years. I anticipate this trend to continue, but management commentary from the Q4 earnings call, their full year 2024 guidance, and the comments from the recent investor conference make it clear that SoFi is planning on being conservative on the lending side in 2024.

Anthony Noto’s comments here from the Q4 earnings call are very instructive (the emphasis is added by me):

We are taking a conservative and pragmatic approach toward our Lending segment revenue, expecting to largely maintain it, given our concerns about the 2024 macro environment as it relates to uncertainty on rates, the economy, and industry liquidity. Therefore, we will manage the Lending segment revenue to be 92% to 95% of 2023 lending revenue. This very conservative view of lending, reflects our choice to limit lending growth below both the much higher level of demand we have had and expect to continue to see in 2024 and the capacity that we have.

At this week’s UBS Conference, CFO Chris Lapointe added, “In our lending business, we are taking more of a conservative approach given the macro uncertainty with respect to rates as well as liquidity concerns across the broader industry.” Later in the same conference he added that, “Looking forward, I think an awful lot would have to change for us to take a different stance on originations over the course of the next 12 months. There's still a ton of volatility with respect to rates.”

I think SoFi is going to intentionally remain conservative not only in their guidance, but also in their execution until the macro picture becomes clear. This is a choice. Since it’s a choice, and since they seem very clear on this direction, I think they’ll be pulling back on originations until banks begin to loosen and greater liquidity returns to capital markets. This may in fact lead to a decrease in revenue in the lending segment in 2024 as guided, although I suspect that the full year 2024 revenue coming in at 92%-95% of 2023 lending revenue is still sandbagged.

The bigger picture

More importantly, however, this stall in lending growth is a symptom of the macro environment, not a permanent change in the business plan. It also further illustrates that SoFi is not growing only as a result of excess capital. In my conversation with Chris Lapointe in December, I asked him specifically about this very issue. I told him that my analysis has shown that originations per member is fairly consistent even as they’ve seen massive member growth (the trend I already included in the above analysis). I then asked him if the macro environment is more normalized in 2025 and 2026 if that trend would continue.

His response was that the demand they are seeing from borrowers is very robust and directionally my analysis is accurate. In a more normalized environment, where liquidity is not so tight, they can make good on that continued increasing demand from their growing member base and lending would return to growth. He also added that the other business segments like home loans and student loans would especially benefit in a lower rate environment.

In 2024, despite a more difficult environment, they will once again use their agile business to adapt to the environment. That means leaning on the technology platform and financial services for growth. The majority of the growth will come from Financial Services, which is anticipated to grow 75% this year. That growth is driven by, you guessed it, member growth. Even in an environment where they not only have run out of excess capital, but are intentionally not deploying all the capital they have, they will grow total revenue by 20% at the low end of their guide. Most banks would kill for 20% revenue growth. SoFi is the most agile and most resilient US fintech in the market, and their growth is not driven by excess capital.

Conclusion

SoFi has been a growth monster for five full years. There are few companies that can claim to have growth at greater than 30% in each of the last five years and a 50% CAGR overall in that timeframe. The list is significantly shorter if you restrict it to financial companies. I am often told that the only reason for that growth is that they became a bank and had excess capital to deploy, but the data tell a different story. They leverage different products and lean on different products to maximize how they grow, but the real driver of their growth is something much easier to track: product adoption. SoFi is at the beginning of its member growth S-curve, having guided for significant growth in the years to come. CEO Anthony Noto put it this way in May, 2023.

You know, we’ve been adding about 400,000 members per quarter, I expect that number to grow. And I think by 2024, 2025, instead of adding 400,000 members a quarter, we could be adding double that, maybe even close to 1,000,000, and so as I think about the scale of our business, it starts with members […] 5 years from now I’d be really disappointed if we hadn’t added a significant number of members […] we could easily be in the 20M+ member range.

Ultimately, growth comes from product adoption and product adoption comes from member growth. If membership triples from here over the next 5 years, you can expect revenue from lending and financial services to roughly triple as well. They are focused on a long term membership CAGR of at least 25%. If they do that, the revenue and the growth will follow.

Subscriber update

I keep inching toward the YouTube channel goal of 100 paid subscribers. I’ve seen a decent boost in the past couple months and I am extremely grateful to those that are supporting the substack.

Right now I am comfortable with taking the time to write about 2 articles every month. Once I get to 100 paid subscribers, I’ll start a YouTube channel and do at least one video every other week (I plan on also posting those on X).

Paid subscribers also get access to a private X chat. If you are a paid subscriber and not in the chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

Disclosures: I have long positions in SOFI and LendingClub.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

A great read as always! Thanks Chris. I agree, to me its the member growth that counts. I keep asking my cousins in Chicago and Texas if they have organically heard about SoFi (other than from me and I am Canadian), and they still say that they only know it as a Student Loan company.

Thanks Chris - this is why the brand awareness drive and holding APY rates higher for longer costs money up front but ultimately attracts members. This aggressive approach is critical in the early years to widen the moat from any other fintechs trying to replicate SoFis business model.