DDI Earnings Prediction: SoFi Q3 Earnings – It's All About the Momentum

For the first time in what seems like forever, SoFi the company and SoFi the stock have seemed to turned a corner. Sentiment has begun to shift and the stock has recently hit multiple 52-week highs. SoFi finally has positive momentum. I don’t really do price targets, but my own evaluation of its fundamentals makes me believe that the fundamentals of the company easily justify a share price in the mid-teens at a minimum. I think this rally can continue to have legs, but next week’s earnings report, guidance, and call will be a pivotal moment to see if the momentum will continue.

Last quarter I thought that SoFi needed to come out swinging and control the narrative around the stock. They did so by sharing extra information they hadn’t before, like they did around loss curves, and by setting the tone in the call. Noto and Lapointe came out with a chip on their shoulder and did a masterful job. I sincerely hope they bring that same energy and swagger to this call. I don’t pretend to know what will happen to the stock after the call, but I believe that if they can combine that enthusiasm with their typical execution, the momentum should continue to drive to higher highs over the next 12 months.

Let’s get into my predictions for this earnings.

Members

Members are the key driver in the customer-facing SoFi business. The faster membership grows, the faster the business grows.

Q3 in 2023 was the largest member growth quarter of all time. It had the advantage of being supported by Taylor Swift performing for six nights at SoFi Stadium. SoFi gives nice perks for members at the stadium, so that almost certainly bolstered new membership. With the exception of that outlier, it’s been a pretty steady upward trend. Their marketing spend might be a little higher this quarter because I think they are leaning back into lending (more on that below), which might also bolster membership numbers. They are also one of the only companies who offer in-school student loans, so that might also contribute to slightly higher membership growth. I think those factors combined will leave them with around 675k new members this quarter.

Originations

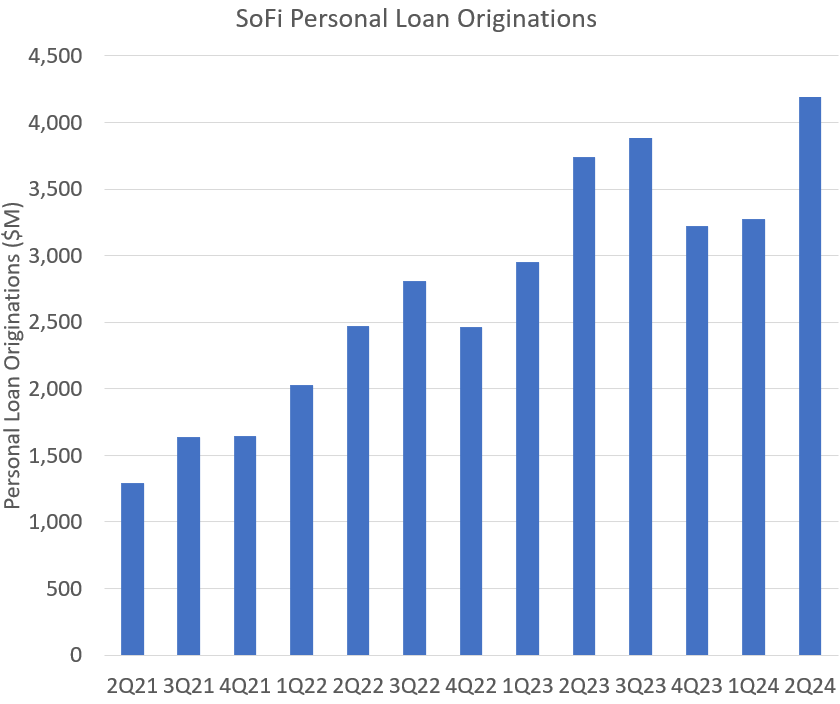

Personal Loans

SoFi started pulling back on originations in Q3 of last year. The trigger to get to growth in the lending business was rate cuts. In Q4 and Q1 they played it very safe as they waited for the macro picture to crystallize. They talked about taking it easy in Q2 as well, and then completely blew all estimates out of the water with almost $4.2B in originations.

By the time Q3 was in full swing, a dovish Fed had emerged and they had all but guaranteed the first rate cut in their September meeting. It turns out it was a 50 bps cut. While I don’t expect the floodgates to completely reopen, I do think that originations will continue to increase. Q3 had been the highest quarter in originations per member in 2020, 2021, and 2022. That did not happen in 2023 because of the intentional pullback in originations, but I expect this Q3 to again be higher than Q2.

I think that it is reasonable to expect at least $500/member of personal loan originations in Q3. Which would end up being $4.72B in originations. If they really got back to a more normal level of originations of around $550/member, it would result in $5.2B in originations. I think they’ll come out closer to the lower end of this range since I don’t think they are going full speed ahead yet. I expect $4.75B in personal loan originations.

Student Loans

Rates moving down will be a tailwind for student loans. Additionally, Q3 is when people return to school and there was a large increase in rates on federal loans. While I do not expect a massive increase in originations, I do think there will be a slight tailwind from in-school loans, resulting in $950M of student loan originations.

Deposits

I was taken off guard last quarter because SoFi let so many time deposits expire without replacing them, resulting in total deposits being lower than I projected. However, what I actually care most about is their demand and savings deposits, because that is their lowest cost capital. I think this quarter they get just over $3B in deposits in checking and savings because of the strength of their member growth. I also think their time deposits will continue to decrease, which I’m fine with.

Revenue

Lending

As I said earlier, I think that we see record originations this quarter for personal loans. Because SoFi uses fair value accounting, they do recognize some of the revenue up front from these originations. SoFi guided for lending revenue to be “at least 95% of 2023 levels” and I think there is not a chance that will happen. I think lending revenue will grow this year relative to 2023. And I think lending revenue for this quarter comes in at $352M, which would be 3% YoY growth.

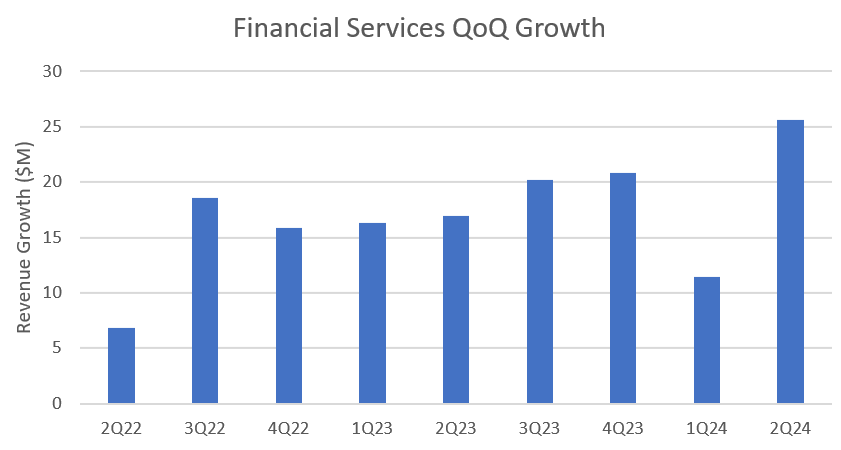

Financial Services

I’m going to be honest here. I know that SoFi usually sandbags their guidance, but I think their Financial Services guidance is a pretty big stretch. They said they will have FS revenue growth of “more than 80% versus 2023 levels”. Total FS revenue last year was $436.5M. 80% growth means they need $785.7M in revenue this year. They only had $326.7M in the first two quarters, which means the back half of the year they need $459M in Q3 and Q4 to make it happen. That means around $210M in Q3 and $250M in Q4. That would be massive growth. Here is their FS quarterly revenue growth.

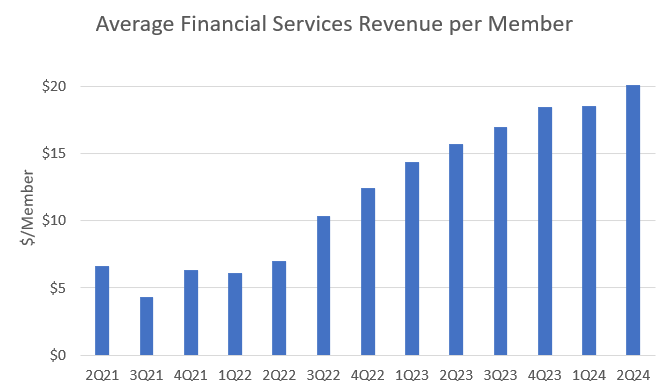

In order to hit their guidance, they need around $34M in QoQ growth in Q3 and then $40M in growth in Q4. That is a very big ask. Average revenue per member probably needs to go from $20/member to $22.20/member this quarter and then around $24.40/member in Q4 to get that kind of growth. While SoFi has made big strides in this regard, a lot of that was from replacing higher cost capital (warehouse lines) with lower cost deposits, boosting their net interest income in Financial Services. That gravy train will be slowing down now as their warehouse lines now have smaller balances. Expanding their balance sheet with more loans would also help, but even still, it’s going to be a stretch to hit that guidance.

All that being said, management has earned my trust, so I’m prediction $210M in FS revenue this quarter.

Tech Platform

Tech Platform revenue has been flat for three straight quarters, and has been disappointing for a full two years now. Growth has completely stalled out and needs to reaccelerate. It’s time to put up real results here. This is the third straight quarter my prediction is $103M in TP revenue, and they’ve let me down the previous two quarters. They absolutely need that as a bare minimum to hit their full year tech platform guidance. It’s time to show results here. No more excuses of long sales cycles and slowly ramping revenue on new contracts. If they want to be the AWS of fintech, they need to start showing growth.

Corporate Revenue

I think corporate revenue now returns to it’s typical levels of being dominated by the interest they are paying on their convertible notes and corporate revolving line of debt. The SOFR (on which their corporate revolving line of credit is based) moved down in Q3 relative to Q2, which means corporate revenue should be a less of a drag than the -$13.7M it was last quarter. I’m predicting -11M for corporate revenue.

Total Adjusted Net Revenue

That makes for a total adjusted net revenue of $654M. The midpoint of their guidance is $635M and analyst expectations are $633.8M. They’ve never missed the midpoint of their guidance and the average beat is $22M of their own guidance. My estimate here is a beat of $19M above their guide. Although as I said, that Financial Services number would be very impressive.

Adjusted EBITDA

SoFi has shown excellent incremental EBITDA margins for several years now. I assume that they’ll continue to do so for the near future. I’m assuming an incremental QoQ EBITDA margin of 55%, which would result in an adjusted EBITDA of $169M. Their guidance is for $162.5M, and analyst estimates are for 167.28M. My estimate is only a very modest beat. They’ve never missed the midpoint of their own guidance and the average beat is $19M.

Net Income and EPS

With the exception of Q4 of last year, which was a quarter that broke every trend across the board because of their push for profitability, adjustments between adjusted EBITDA and net income have hovered right around $120M for the last two years or so.

I expect a similar amount this time, so I’m prediction $49.3M of net income. Fortunately, all the preferred shares have been retired so we won’t get weird dividend payments subtracted from the net income when calculating the EPS. I’m assuming 1.08B average shares outstanding, which leaves $0.046 cents of EPS, which rounds up to $0.05. Analyst estimates are for $0.04, so this would be a small beat.

Guidance

The midpoint of SoFi’s yearly guidance and Q3 guidance implied a Q4 guidance of $632M, which would be slightly down from Q3. Similarly, their yearly guide for EPS was $0.095 at the midpoint, implying that Q4 EPS was expected to be $0.025, which would also be a decrease from Q3. Analysts are predicting $641M and $0.03, respectively. Given their aggressive Financial Services guidance, the fact that I expect they are leaning back into lending, and the $2B forward flow agreement they just announced last week, I can’t see Q4 being worse than Q3.

They will once again raise their guidance. I expect that it won’t be too far beyond what they do in Q3. Predicting their guidance is even harder than predicting results, which I also almost never get correct, so take this with a grain of salt, but I predict their revenue guide will be for $665M at the midpoint, their adjusted EBITDA guidance to be for $170M, and EPS to be $0.05.

Commentary

Last quarter, I was concerned about NCOs and delinquencies and while I thought that the fears from analysts like KBW were overblown, SoFi’s actual NCO results were monumentally better than what people, including myself, were predicting. Delinquencies actually came down last quarter, so I’m optimistic that we will see NCOs top out this quarter. While I think the risk here is lower than it was last quarter, I do think that analysts will be keen to see if there is any weakness.

From a narrative standpoint, I think the most important thing is maintaining momentum. The quarter and guidance I predicted here I would think would justify the recent run and see continued momentum if paired with enthusiasm and a positive outlook in the call. I honestly think that SoFi might have some product updates that they talk about in the call. They don’t always do that, but I think they might talk about their updated SoFi Plus rollout, we’ll probably get commentary on the credit card beta program, and they’ll probably give more detail on the $2B agreement with Fortress.

Predictions in one place for easy reference:

Members: 675k New Members

Personal loan originations: $4.75B

Student loan originations: $950M

New deposits: $3.0B

Lending revenue: $352M

Financial Services Revenue: $210M

Technology Platform Revenue: $103M

Corporate Revenue: -$11M

Total adjusted net revenue: $654M

Adjusted EBITDA: $169M

GAAP Net Income: $49M

GAAP EPS: $0.046

Subscriber update

I am right on the cusp of starting my YouTube channel. I just need a few more paid subscribers to get there.

Paid subscribers get three perks.

1) Access to a private X chat.

2) I buy stocks every week, and every week I send out my weekly DCA weighting list to subscribers

3) I send out a portfolio snapshot at the beginning of each month which shows my total allocation to each of my positions.

If you are a paid subscriber and not in the X chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

Disclosures: I have long positions in SoFi.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

A couple of comments with regards to how you see each vertical:

Lending:

- I looked at comps with other banks (student loans: Discover Q3; personal loans: Discover and Capital One Q3)

- Based on the trends observed by those banks, and SOFI's own trends in the last Qs, it is plausible to expect estable/positive growth this quarter. I am unable to say magnitude (it would be interesting to see your assumptions for that 3% growth), but in general this seems logical

Financial Services:

- Here, I partially agree/disagree with you. I am more positive with regards to this vertical. QoQ and YoY trends clearly show that this is where growth is taking place at SOFI. Credit card growth has been healthy, and industry peers are not showing red flags in terms of credit issues. I could be wrong, but if SOFI beats this quarter, this vertical might be a posible explanation

Technology:

- Of the 3 verticals, this is the one I am the least bullish. It is already 4 years since SOFI acquired Galileo. This would have been a prudential time for them to show better growth and results. Growth rate is modest. Can it change over time? Maybe. A major announcement of a deal with a large institution could change direction.

Overall, I would expect some beat considering that the vast majority of banks have done it, and comparables in Consumer Banking segments by other banks have been healthy. I could be completely wrong, of course!

Disclosure: No position (I might trade long and short via options on extremes. Also, I might consider a long position in 2025 if Financial Services keep growing)

PS last q they rounded 1.6c down to 1c - if I'm correct? Hope they don't do that again