Q1 2025 Earnings Preview: Smooth Sailing Ahead

This is probably the quarterly earnings I’ve felt the most calm about since covering SoFi. The stock is down, expectations are not particularly high, analyst estimates are very low, sentiment is low, and the data we’ve received during the quarter is positive. In 2022 and 2023, every single quarter was an absolute fight for the company’s life with bears lambasting the rising delinquencies and stoking the fires of fair value fears. In 2024 people were either wondering why everything was running except SoFi (Q1 and Q2), or concerned it had run too hard and was due for a sell-off (Q3 and Q4). Now it feels like the pressure is mostly off and my only question is how big of a beat SoFi puts up.

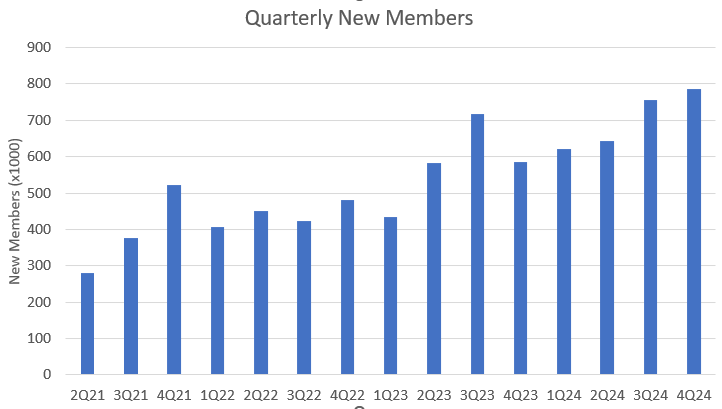

Members

Maybe the single most interesting data we got this quarter is website data. Between NBA, TGL, and their other marketing channels, it appears from the data that SoFi’s marketing is crushing it.

January traffic passed the previous all-time high by almost 3M visits (19.53M vs 16.72M). February, even in a short month, had almost 18M visits, and then March blew it out of the water even further with 21.19M visits. That looks like some bullish numbers for new members. SoFi said they were going to reinvest for growth in 2025, and this looks like an example of that happening. Member growth has been fantastic and looks to be continuing that trend. Between that and the potential leak of 11M members that popped up on their recent new job listings I’m expecting the first 900k+ member quarter with 903k new members.

Originations

Personal Loans

This is really hard to figure out because of the Blue Owl Capital deal. On January 27 on the Q4 earnings call, SoFi said they “agreed to initial terms with Blue Owl Capital Funds for up to $5 billion of personal loans over two years”. We didn’t get actual confirmation of the deal until March 13. But the Fortress deal from last year wasn’t actually announced until October 14, 2024 but we found out they’d been originating loans from them starting at the beginning of Q3 four months earlier. The Blue Owl Capital deal is $625M per quarter in originations. Even if this deal only started on March 13, that’s around $130M of originations in the quarter. If they started originating in January or February, the number is much higher.

Either way, SoFi now has the capital and growth in tangible book value to support modest growth in their balance sheet while simultaneously growing originations through the LPB. I think originations set another new high at $5.7B, but that could be anywhere from $5.4B to $6.0B depending on when that deal went into effect. This will fuel growth in Lending revenue from rising net interest income from loans on the balance sheet, noninterest income through recognized fair values. It will also fuel Financial Services growth through the Loan Platform Business.

Student and Home Loans

Last quarter surprised me with $1.35B in student loans and $577M in home loans. Rates have been fairly steady since then, and the real estate market has been pretty poor in Q1. Student loans might get a bigger bump in Q2 now that the new administration is starting to refer defaulted payers to collections, but I have a hard time getting a feel for Q1. I think both these numbers will come down slightly with $1.3B in student loans and around $450M in home loans.

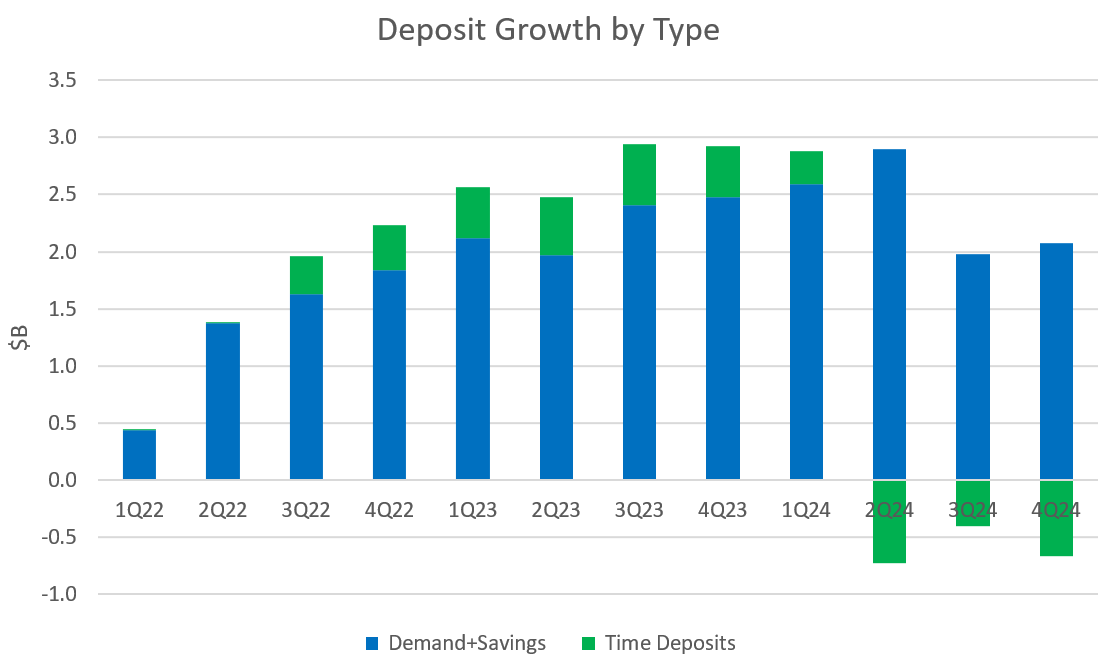

Deposits

SoFi has pretty much reached their deposit goals, with over 90% of their loans backed by deposits, so they aren’t going to really push here. The lower APY they’ve been offering (from a peak of 4.6% to its current level at 3.8%) has been mostly in line with competitors, and the ecosystem benefits are high enough for them to still retain users. They can monetize deposits even after 100% of loans are backed by deposits, but not at as high of a net interest margin.

I expect them to let more time deposits run off without replacing them and that demand and savings deposits (demand deposits are the same thing as checking deposits) will continue to grow at a modest pace, probably at around $1.8B. I may not be covering these as closely in the future unless we see a big change in the trend here. SoFi will continue to grow deposits along with members, so member growth is a more important metric to track.

Revenue

Lending

I still think SoFi will grow lending beyond the 15% CAGR they outlined for 2023-2026. Last year lending grew 11%, but remember that they really throttled originations in both Q4 2023 and Q1 2024, leading to a couple of very low growth quarters at the beginning of 2024. Also, their net interest income (the blue bars), now make up the vast majority of lending revenue, while noninterest income (green bars) is no longer a large contributor. I think it’s instructive to focus on what is going on with net interest income to figure out how lending revenue is going to move.

SoFi now has enough retained earnings to be able to continue to grow their loan book without changing their capital ratios. That means they can sustainably add hundreds of millions of loans to their balance sheet without having to worry as much as they did before they were profitable. More loans held means more interest income recognized.

Moreover, they’ve been slowly reducing the APY they are offering.

August 26, 2024: APY reduced from 4.60% to 4.50% (a decrease of 0.10%).

October 7, 2024: APY reduced from 4.50% to 4.30% (a decrease of 0.20%).

October 30, 2024 : APY reduced from 4.30% to 4.20% (a decrease of 0.10%).

December 2, 2024: APY reduced from 4.20% to 4.00% (a decrease of 0.20%).

January 23, 2025: APY reduced from 4.00% to 3.80% (a decrease of 0.20%).

The average APY in Q4 was around 4.15%. In Q1, it’ll be around 3.85%. Average savings deposits well be around $22.5B. That 0.3% difference in the rate they are paying out for deposits translates to around $17M more in revenue, all else equal. That’ll get split between Lending and Financial Services, but it means that net interest margin (NIM) for each type of loan will be expanding this quarter. I think lending revenue expands from $423M last quarter to $440M this quarter.

Financial Services

Expanding LPB business, lower APY on savings accounts, continued cross sell, and a huge quarter of member adds will all be tailwinds this quarter. Here is the average financial services revenue per member for SoFi.

Assuming it drops just a tiny bit from last quarter again, which is probably a conservative assumption, to $25.20/member, and with the huge member adds I’m predicting, this quarter ends up with FS revenue of $277.2M. That’s about a $20M increase from last quarter’s $256.5M. There is room for upside here if the Blue Owl Capital deal was implemented earlier in the quarter than March.

Technology Platform

I’ll believe in the growth here when I see it. We haven’t seen it yet, and Q1 is historically slightly weaker for the Tech Platform. I still am projecting very modest QoQ growth as we are hopefully moving from fintech winter into fintech spring. Last quarter was $102.8M, and I’m projecting $105M for Q1. I’d love for them to highlight any new deals signed like they did in Q4, that was really interesting and useful info.

Corporate

Continues to be impossible to predict, so I’m keeping it close to flat QoQ at -$40M. Be aware that if this number is lower, like if it comes in at only -$20M, that may mean my projections for Lending or Financial Services are slightly too high, since all this balances in the Funds Transfer Pricing framework. It’s complicated, but at the end of the day doesn’t matter too much.

Total Adjusted Net Revenue

That puts my prediction for ANR at $782M. SoFi’s guidance was for $735M at the midpoint and analyst estimates are at $739M at the time of writing. I think there is no possible way they miss their guidance or analyst estimates. If my estimate is correct, this also represents 34.7% YoY revenue growth, which would be a truly impressive number.

Adjusted EBITDA

To get those big revenue numbers and add that many people into the ecosystem means that there will be some extra reinvestment into the business required. They outright said to expect lower incremental EBITDA margins in the 30% range in their last earnings call. I’m assuming slightly better than that at 34% YoY and 35% QoQ, which puts my estimate at $213M. Analyst expectations are $173M and their guidance was for $180M, so this would, again, be a sizeable beat.

Net Income and EPS

Using what I think are suitable estimates for the differences between EBITDA and net income and using a tax rate of 30%, I get a GAAP net income of $54.6M. They said their assumed tax rate for the year would be 26%, but they have a higher tax burden in the first few quarters because of payroll taxes for social security, so I bumped it up to 30% for this quarter. Their own guidance and analyst estimates are for $0.03. My estimate puts them at $0.047, which rounds up to $0.05.

Guidance

If there is somewhere that SoFi might fall short, it will be guidance. They’ll raise the full year guidance, but the Q2 guide might look a little weak compared to analyst expectations. In three of the last four quarters, SoFi has had a sizeable beat, but their guidance for the next quarter was actually lower relative to what they just delivered. That may happen again here because they are so conservative on guidance and because there is so much uncertainty regarding the macro right now. SoFi has proven they’d rather guide low even if the stock suffers. This is the one part of the earnings that could miss and might end up with the stock being punished. Analyst expectations for Q2 are $791M, which is higher than I’m seeing for this quarter’s results, meaning if they do have a slightly downward guide like they are prone to do, they’ll miss. The stock may get unfairly punished for this again.

Bonus Prediction

We’ve seen hints in the app code for Cash Coach, Crypto, and additional options work in the last few weeks. I think there will, once again, be a new product announcement on the earnings call. People have been criticizing them for a lack of innovation, and this would be a good opportunity to show that isn’t the case.

Conclusion

This will be another steady and extremely strong quarter from SoFi. Most companies would kill to see 30% growth. SoFi will almost certainly eclipse that number, show strong results, reinforce the growth in the LPB, and generally show that its fundamentals just keep improving. They will almost certainly have record new member growth as well. SoFi has become a stock that I can sleep easy at night holding. Quarter after quarter they put up excellent, consistent, durable, sustainable growth. This quarter will be no different. I don’t know how the stock will react and I don’t particularly care. The company is just continuing to execute and this quarter will be no different.

Subscriber update

The DDI YouTube Channel is live. I’m still figuring out how to do everything there, but expect to see more as we go. A sincere and heart-felt thank you to those who support my work. If you do want to support my work, there are several ways to do so. You can subscribe here on substack, or on X, or, now, on YouTube.

Paid subscribers get three perks.

1) Access to a private X chat.

2) I buy stocks every week, and every week I send out my weekly DCA weighting list to subscribers

3) I send out a portfolio snapshot at the beginning of each month which shows my total allocation to each of my positions.

If you are a paid subscriber and not in the X chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

You can also use my referral links for SoFi if you want free money when you sign up for SoFi, or discounts on Tesla or finchat.io:

SoFi Money Link - Get an extra $25 when opening an account

SoFi Invest Link - Get an extra $25 when opening an account

Tesla Referral Link - Get up to $2500 off a new Tesla

finchat.io Link - Get 15% off

Disclosures: I have long positions in SoFi

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Excellent article, Chris. As always!

I am worried about them closing any more deals with LPB this year. All of the soft data is pointing to a very painful retraction. Manufacturing and transportation falling through the floor. Small businesses are about to be hammered. I would not want to be buying personal loans except from the top box that Sofi currently keeps to themselves. Guidance will be very interesting. On the other hand Sofi may do awesome in an environment where small and medium size banks get hammered.