SoFi Q1 2024 Earnings Review: A Good Quarter but a Few Questions Remain

I said this quarter was going to be the hardest one to predict so far. It was also, in my opinion, one of the more underwhelming quarters that SoFi has had, but that is only because they have set a very high standard. Last year’s earnings reports were excellent across the board, and Q2 and Q3 were especially exceptional. Q1 of 2024 was a good quarter, but there were several aspects of it that are kind of “meh”. I’ll go back through my predictions, compare them to the actual results, and try to frame the results from that discussion.

Members

Long-time readers know that I think member growth is one of the the key long-term drivers for SoFi’s business. SoFi beat my expectations for member growth by a decent amount. I thought they’d get 595k new members and they ended up with 622k new members.

Marketing efficiency continues to improve as well. Sales & marketing expenses decreased for the second quarter in a row and it is actually down to a level not seen since Q3 of 2022. For reference, SoFi spent $162M on S&M that quarter and only grew members by 424k. This quarter they spent $167M and added 622k. That’s almost 50% more new members for the same ad spend. It really speaks to the improved leverage they are getting from each marketing dollar spent. Management attributes this to unaided brand awareness from deals like the SoFi stadium and NBA partnership. The numbers are backing up that commentary. Many were concerned about the cost of the NBA deal, which started in mid February. The fact that S&M came down in Q1 shows that the cost does not seem too significant. Customer acquisition cost has very definitively come down since peaking one year ago.

Before we leave the discussion of members, it’s important to point out that they are now subtracting out removed members from their total member counts. If you take last quarter’s total members and add this quarter’s new members, you do not get this quarter’s total numbers. There was a footnote about this in the presentation:

Beginning in the first quarter of 2024, new member and new product addition metrics for the relevant period reflect actual growth or declines in members and products that occurred in that period whereas the total number of members and products reflects not only the growth or decline of each metric in the current period but also additions or deletions due to prior period factors, if any, described in footnotes 1 and 2 above.

The difference between the new member adds and the total members was 32k. That is the total members removed not just from Q1, but from previous quarters as well. Members removed should be smaller than this in future quarters. 32k is fairly immaterial to the overall member count of 8.1M members. It will be interesting to track this number moving forward.

Originations

My expectations for personal loan originations were once again too high. I was wrong with my read of the situation regarding how they might use the excess capital they raised in Q1. SoFi really has completely taken their foot off the accelerator in personal loans. I predicted $3.65B in originations and they came in at $3.28B. This was in spite of the fact that they sold $1.26B in personal loans, which was in the range of $1.1B-$1.8B that I expected, and increased tangible book value by $608M (about $500M from the convertible note exchange and about $100M from business operations).

They have plenty of excess capital now. As a result of the convertible note deal and the organic increase in tangible book value from continued operations, capital constraints are not a problem and will not be for the foreseeable future. In spite of this, originations were basically flat from Q4 levels. Unused capital is money left on the table from a returns standpoint. SoFi has made a strategic decision to wait until there is more clarity on where rates will be moving before deploying that capital. I think they are being overly conservative given the amount of capital buffer they have, but I have no practical experience in risk management or banking and I’m not an economist, so I trust their judgement.

Moving forward, I am aligning my own expectations with management’s guidance. They have put the lending segment on cruise control and until they definitively say they are shifting their stance and reaccelerating originations again, I will assume they are going to remain very conservative. I did not previously truly think that lending revenue would be down this year relative to last year, but it is now apparent to me that that is how they will execute the business.

Deposits

SoFi had their strongest deposit increase ever in Q1. This is a testament to the fact that they continue to add users and users continue to switch and make them their primary bank. They added $2.98B deposits, which was under my estimate of $3.1B, but was a new record for deposit increases in a quarter. Average deposit per SoFi Money product (Checking & Savings accounts count as Money products) also increased slightly from $5,519 to $5,568 in the quarter. Deposit growth is driven by the fact that they are adding members and existing members are adding more deposits to the platform.

SoFi actually had the highest deposit growth of any large digital bank. Discover and Ally both had very weak quarters in terms of deposits added. It was Discover’s weakest quarter in two years. The other banks deposit growth trends are fairly correlated to each other. When one bank has a good deposit quarter, the others tend to as well. SoFi remains uncorrelated to the other banks and grows deposits at a very steady rate that is continuously increasing.

Revenue

The segment revenue is the bad part of this earnings. SoFi came in underneath my own personal predictions in all three core business segments. I’ll go through them individually.

Lending Revenue

Personal loan originations, which is the driver of lending revenue for the time being, came in well below what I expected as covered above. That inevitably led to lower revenue than my predictions as well. SoFi is deliberately leaving revenue on the table in lending. They have been very clear about the reasons why. In the near term it is hurting the company’s growth, and there is no clear timeline for when they will deploy the capital they have. Noto addressed this during the Q&A portion of the call.

We went into 2024 with a view that our growth would be driven by the combined impact of Tech Platform and Financial Services businesses. Those businesses are now big enough in terms of total scale and profitable enough that we could put our resources behind them and still grow as we did this quarter over 26% year-over-year, while the lending business was essentially flat year-over-year. Our decision to make that transition in 2024 wasn't driven by capital. We had excess capital and could grow it much faster. We have even more excess capital now but our stance hasn't changed because that wasn't the reason for keeping it relatively conservative. […] We started in October, talking about higher for longer. While the market and different government officials led people to believe there'd be six rate cuts at one point. Now we're down to one to two rate cuts. We think we took the appropriate stance, and we're well positioned to play where the economy goes in 2024.

Growth in lending is on hold until the macro becomes more clear. That is a fact of SoFi for the near term, and when I say near term, it could mean all of 2024 and even into 2025. Fortunately I invested in the company and I’m not just trading the stock. I am ok with them taking a prudent approach in the short term. There will come a time when the economic picture becomes more clear and SoFi will lean into lending growth and go back to the 14%-15% range on their capital ratios, which would mean growth in both net interest income through more loans on the books and non interest income through originations. Many SoFi detractors were absolutely convinced that without lending growth the company would crater. 26% overall revenue growth on flat YoY lending revenue tells a different story. I’m comfortable waiting for a return to lending growth even if it takes years. Others might not be, and that is ok.

Regulatory fears

A bearish alternative explanation for the decline in revenue growth is that regulators are forcing their hand. I have seen the argument made that the excess capital raise from the convertible notes deals was mandated or heavily encouraged by the Federal Reserve, FDIC, or the OCC, and that SoFi is not doing this as a choice but as a requirement. One of the questions in the Q&A was from Jeffrey Adelson from Morgan Stanley, who asked “Then I guess the comments on keeping your excess capital this year in light of the macro uncertainty. Are you hearing anything from your regulators on there about any sort of buffer you might need to keep?”

Noto’s response was, “So what I'd say is we 100% have the option to drive the lending business faster if we'd like. […] We have excess capital well above we started the year with at 17%. So we have the option to grow the business much faster if we choose to.” While I can never be completely certain, I’m very confident that SoFi’s decision to pull back on lending is self imposed. It is a choice. Their hand is not being forced by regulators. I asked IR this same thing and they also said that the capital raise was not driven by regulators. This argument will probably persist, but I think Noto was clear on the call and IR was clear in their communication and I don’t think this argument holds any water.

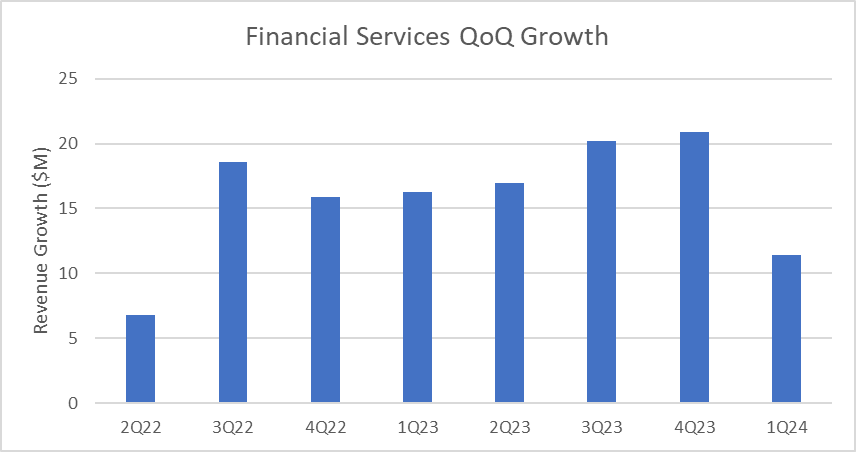

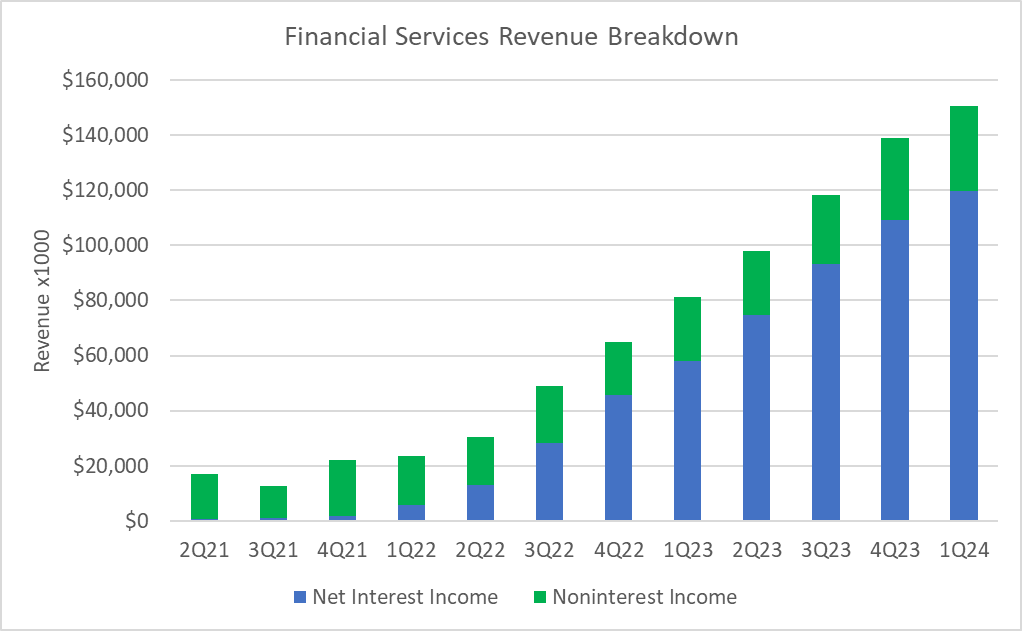

Financial Services

I have no idea why FS growth was only $10M this quarter where it has been $20M every quarter for well over a year. Most of the financial services growth comes from net interest income, which is driven by deposits. Deposits, as we covered above, grew by a larger amount in 1Q 2024 than any previous quarter, so I would have assumed that FS revenue likely would have grown by more. A portion of this was explained by the network fee issue that gave them a little extra boost in Q4, but it seems to me that the financial services net interest income growth should have been higher.

I am hoping that the 10-Q will shed more light here than we currently have. It seems to me that the most likely explanation is that the internal rate that Financial Services charges the Lending segment for their deposits decreased slightly in Q1 relative to Q4, but I am unsure on why that would be the case since rates did not move too much in the quarter. I’ll discuss this a little more in the corporate revenue section below.

Technology Platform

This quarter’s technology platform results highlight the fact that analysts and investors need better metrics and clarity in this part of the business. It is really frustrating to me that there is still so little information available about Galileo. Beyond revenue and Galileo accounts, there is nothing of use that they publish to be able to gain greater insight. We still have no idea how many banks are using their core technology, how the core product and payment processing are progressing on cross selling, or how many financial institutions are using the payment risk platform or Konecta.

For example, I was initially disappointed with the tech platform revenue decreasing from Q4 2023 to Q1 2024. Last year there was a drop between Q4 2022 to Q1 2023 as well. However, they lost their second biggest client, Current, in Q4 of 2022, so I attributed the lower revenue to the simultaneous decrease in Galileo accounts from Current. The year before that, from Q4 2021 to Q1 2022, tech platform revenue had increased. That was during a period of very rapid account growth for the business because neobanks were thriving. Just as importantly, they closed the Technisys acquisition part of the way through the quarter, so the extra revenue from Technisys masked the seasonality trend.

This was also addressed in the Q&A, where Noto said “Q1 is a seasonally weaker quarter for the Technology Platform business, but the year-over-year growth rate is what people should focus on because that eliminates the impact of seasonality and that accelerated.” There are only a small handful of people who have followed this company as in depth or as long as I have. Since it still traded under the ticker symbol IPOE, I don’t think I have missed anything that they have said publicly, and this is the first time I remember hearing about seasonal weakness in Galileo’s business. It makes sense that a payment processing company would see seasonal weakness in Q1 as spending in general does decrease relative to Q4. Maybe I missed something, but the fact that nobody else seems to have seen this coming either leads me to believe I was not the only one who was unaware of the inherent seasonality in the tech platform. I think this is something that was missed by analysts and investors alike.

However, if the revenue was broken down into categories like payment processing, banking core, and others, this would have been an obvious trend to predict. Instead, I assumed there would be account growth this quarter (which was correct), and that that account growth would lead to revenue growth (which was incorrect because of the seasonality). Instead, I was left confused by the results I saw and disheartened by the perceived weakness in such a core part of the business until it was cleared up in the earnings call. If I’m that confused, it is a safe bet that other analysts and institutional investors were as well. I’m also left with egg on my face because my prediction of $103M in revenue was way off. I’ll do better and account for seasonality in the future, but it sure would have been better to know this ahead of time. I’ve been asking for better and more information about Galileo for a while now and hope it comes soon. I think investors deserve it.

Corporate

Corporate revenue, for the second quarter in a row, came in well in excess of my personal expectations. I have reached out to IR and hope to get more clarity here because I really want to better understand why this line item is so volatile between quarters. It was -$20M for four quarters in 2023 and had been negative for eight straight quarters before swinging upward to around $10M for the last two quarters. The biggest difference by far is in the net interest line. It is possible they have slightly changed the way that they are accounting for things in their FTP framework, which would also help to explain why Financial Services net interest income was lower than I expected to see.

At the end of the day I am not really concerned about how much the extra revenue from deposit growth is spread between financials services vs lending vs corporate. However, I do want to understand how the improvement in the core business drives overall results of the company, and right now there are still some questions I don’t have answers to. A $20M-$30M swing is enough to have a sizeable effect on the quarterly results and easily cause a miss or a beat in any individual quarter. It’s important to me to know if this is because of the business, or if it is because of one-off occurrences. While each quarter this becomes a smaller portion of the overall revenue mix and eventually it will be lost in the noise, it is still important for the next several years and needs to be better understood.

Total Adjusted Net Revenue

Headline numbers (total adjusted net revenue, adjusted EBITDA, GAAP net income, and EPS) were really good. While they were all sequentially down from Q4, that is to be expected because SoFi did everything they could to be absolutely positive they would be GAAP profitable in Q4. A slight decrease was both guided for and expected.

While each individual segment was lower than what I had predicted, corporate revenue was a lot higher than I thought it’d be and in the end my prediction of $585M in total adjusted net revenue was very close to the actual $580M that they generated. The corporate revenue line here is very important. We need to know whether the increase is due to core business operations or if it is one-off line items. Again, hopefully either the 10-Q or a response from IR will help to shed some light on this matter.

Adjusted EBITDA

Lending margins were still excellent. I thought tech platform margins would fall but they actually improved slightly. What’s more, financial services continues to prove that it is mostly a fixed cost business, that the variable costs are low, and that most of the revenue growth goes straight to the bottom line. In fact, FS revenue growth was only $11.4M but its contribution profit increased by $12.1M. Profitability actually increased by more than the increase in revenue, as expenses in the segment decreased between Q4 and Q1. This more than likely was a result of the decreased sales and marketing spend that was described above in the members section.

Overall, better margins across the board meant more adjusted EBITDA than I expected. I predicted $126M and SoFi ended up with $144M. They continue to show that their long term EBITDA margins are probably going to end up above the long term 30% EBITDA guidance they have provided. This is the sixth straight quarter that their trailing twelve month incremental EBITDA margins are above 40%. Noto, in a prior life as an analyst, used this as a forward indicator of where the margins would end up in the businesses he analyzed. If it is a forward indicator for SoFi, it is a very positive one. The numbers are undoubtedly buoyed by the drive to profitability in 2023, and will more than likely come back down in the coming quarters, but this will be a key number to watch moving forward, especially into 2025.

GAAP Net Income

My prediction for GAAP net income was equivalent to $16M in diluted GAAP net income. SoFi came in with $22.5M, beating my prediction by $6.5M and also beating analyst estimates. They continue to drive margins in the right direction. They’ve guided for that to continue and I expect nothing less.

EPS

Fully diluted weighted average common stock outstanding was 1.042B, leading to EPS of $0.0215. Again, this was above my own estimates of $0.015 and analyst estimates of $0.01.

Conclusion

This quarter was a good one for SoFi. The big picture is that they are still on track to hit their growth guidance of 20% in the tech platform and 75% in financial services. They also firmly established that their decline in lending revenue is a choice and I am adjusting my expectations to align properly with that reality. Unless something really materially changes in the economy in the next 3-6 months that brings clarity to the macro picture, they will not accelerate lending and it seems inevitable that there will be an annualized revenue decline in that segment. I’m not enamored with that prospect, but I accept it and it does not change the long term thesis. The path forward is that SoFi will continue to compound, it will continue to take market share and grow membership, new business lines will be added, the tech platform will bring a capital-light growth vector to the banking side of the business, and they are building a company that is meant to grow over decades.

More analysis to come.

Subscriber update

Right now I am comfortable with taking the time to write about 2 articles every month. Once I get to 100 paid subscribers, I’ll start a YouTube channel and do at least one video every other week (I plan on also posting those on X).

Paid subscribers also get access to a private X chat. If you are a paid subscriber and not in the chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

Disclosures: I have long positions in SoFi and LendingClub.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Curious how they report customers on the tech side. I hear Noto talk about implementations taking quarters - does that mean a customer isn’t reported to the street until their project goes live? I work for a tech firm and afaik we report customers when they sign.(6-9 month implementation not uncommon)

Great read Chris, thanks for your efforts in producing this thorough analysis breakdown.