SoFi Convertible Notes: the Good, the Bad, and the Stock Price Reaction

Recently, SoFi engaged in two separate transactions that they announced at the exact same time. Both of them were regarding senior convertible notes. This was a complicated transaction and there are both positives and negatives. I’ll do my best to lay out the facts of the transactions, and then give commentary on what is good and bad about each part. Also, the deal changed several times due stock price movement and other things (e.g. they originally said they would raise $750M with an option of offering an additional $112.5M which was taken and so they ended up offering $862.5M). The dust has completely settled on everything, so I’m going to use the final values wherever possible. Let’s lay out the facts first. I will try not to get too far in the weeds on this and make it understandable for everyone, but this is going to be one of my longer articles, so buckle up.

What is a Senior Convertible Note?

First things first, let’s define what these are. A senior convertible note is debt that a company takes out to finance their business operations. Senior just means that it has priority to other debt, so if the company goes into bankruptcy, these guys get paid back first before some other types of debt and equity holders. In the recent offering, institutions gave SoFi $862.5M, and SoFi will have to repay that money. That debt has interest that has to be paid by the business, and the full debt has to be repaid in 5 years in either cash or in shares. The intent is for it to be repaid in stock rather than cash. That is what is meant by convertible. The debt can be converted into shares as long as certain conditions are met.

How do the notes convert into shares?

I’ll use a simplified scenario to explain how these notes can convert into shares. Let’s assume that Great Company offers $100M in convertible notes at 1 percent interest to Awesome Institution. Great Company’s stock is trading at $10/share. The conversion price of the notes is 130% of the stock price on the day they were issued. In this case, that is $13/share. So that means that Awesome Institution can, in theory, convert their debt into 7.7M shares of Great Company. The 7.7M shares is $100M/$13.

There is a stipulation though. In order for Awesome Institution to convert the debt to shares, Great Company’s stock has to be above 130% of the conversion price (which is $13). In this case, that is $16.90. Let’s say it hits that price in five years. If it’s above that price, Awesome Institution will happily trade their $100M in debt for 7.7M shares because those shares would be worth $130M on the open market at a price of $16.90 (7.7M x $16.90 = $130M). Great Company got the $100M it needed in capital, Awesome Institution ends up with a 30% return in 5 years if the stock gets to the redemption price, the stock is up 69% so shareholders are happy, and everyone wins. However, the 7.7M shares are dilutive.

Capped Calls

This part will only truly make sense if you understand options trading, but the takeaway is that companies who offer senior convertible notes will use a portion of the money from the cash raised to buy capped calls. The capped calls are meant to reduce the amount of dilution that actually takes place. You can skip the rest of this section if that’s all you want to know and don’t want to get into the details of the options. Here again, is a simplified example of how it might actually work.

After the transaction above, great Company uses $10M to buy capped calls that have a strike price of the conversion price ($13), and a “cap” at double the current share price ($20). They buy enough calls to cover the same number of shares they might be diluting (in this case, they will buy 77k contracts to cover the 7.7M shares). For options traders, a capped call is very similar to a bullish call spread, but both legs will automatically be executed if it reaches the cap price of $20/share. Just like a bullish call spread, the value of the contracts goes up as the share price increases up to the cap.

Using the same hypothetical scenario above, let’s say 5 years have passed and the stock is at the redemption price of $16.90/share. Awesome Institution redeems their notes for 7.7M shares. However, Great Company has capped calls. The capped calls are worth $3.90/contract ($16.90 minus the strike price of $13), which means they are worth $30M in total, and that money can be used to offset dilution.

In effect what this does is it moves the conversion price from Great Company’s perspective from $13/share to $16.90/share, so Great Company only has to deliver $100M/$16.90, or 5.9M shares. The remaining 1.8M shares are effectively paid for by the capped calls. Dilution is reduced from 7.7M shares to 5.9M shares for existing shareholders. This would happen all the way up to a stock price of $20/share, at which price, Great Company would be required to issue 5M shares and the remaining 2.7M shares would be paid for by the capped calls. If the stock price goes above the capped call price, Great Company has to foot the bill of the difference and dilution would increase back up to a maximum of 7.7M shares.

The big picture takeaway is that Great Company is buying capped calls to protect current shareholders against dilution from the conversion price of $13/share all the way up to $20/share, which is double the $10 share price on the day the convertible notes were offered. SoFi, similarly, has entered into capped calls that can decrease dilution to shareholders.

What exactly did SoFi do?

Ok, so now let’s go through SoFi’s transactions.

2029 Note Offering

SoFi announced two transactions at the same time on March 5. They both have to do with senior convertible notes. Let’s cover these one at a time and I’ll try to use the same language SoFi did in their press releases in case anyone goes back to review them. The first part is fairly straight forward; SoFi offered convertible notes to investors worth $862.5M that pay an interest rate of 1.25% (again, this was originally $750M, but I’m using the numbers from the finalized deal). This part of the transaction I will refer to as the “offering” and those notes I’ll refer to as the “2029 notes” because the debt has to be repaid by March 2029.

Since the stock price closed at $7.27 on March 5, the shares have a conversion price of $9.45. That means the $862.5M can be converted to 91,269,841M shares of SoFi stock. Additionally, SoFi used around $90M of the cash they raised to purchase capped calls equal to the 91.3M shares associated with the transaction. The capped calls have a strike price of $9.45 and a cap of $14.54. Of the $862.5M that was raised, the net proceeds from the offering were $845.3M (so they paid about 17M in fees, costs and expenses relating to the transactions). They also used ~$90M to buy capped calls. So the cash that SoFi raised that can be used from this transaction was ~$755M.

2026 Note Exchange

The second part is a little more confusing. Back in October 2021, SoFi raised $1.2B with a senior convertible note offering. Those notes I’ll refer to as “2026 notes” because that debt matures in October 2026. They’ve already repaid some of that debt, so only about $1.1B is remaining. SoFi is paying back $600M of that debt, but they aren’t doing it with cash, they are doing it by exchanging that $600M of debt for $529.5M of SoFi shares.

The first question to answer is, why can they pay back $600M of debt for only $529.5M in shares? These notes, just like anything else in financial markets, can be bought and sold. The 2026 notes have a nominal interest rate of 0%. Their conversion price is $22.41. That is way higher than the current stock price and statistically it is unlikely to convert. 2026 note holders have their capital tied up until October 2026 earning no interest in an environment where they could be getting 5%+ interest risk free. That means the notes, on the open market, are worth less than their face value. SoFi was able to buy them back for 89 cents on the dollar. That’s where the $529.5M in shares comes from, it’s 89% of $600M.

The original estimate of the number of shares required for the exchange was 61.7M. However, the number of shares was dependent on SoFi’s stock price over about a three-week period between March 5 and March 22. SoFi’s stock price was very weak during this time (more on that below), and the volume-weighted average price during this period was $7.29. This resulted in 72.6M shares of SoFi stock being exchanged for $600M in debt since $529.5M / $7.29 = 72.6M.

Now that we’ve laid out the facts, let’s dive into the ramifications for the business and the stock. Again I’ll try to separate out what are facts from what is my analysis or speculation.

Negatives

Dilution

72.6M shares is a lot of shares and a lot of dilution. Total shares outstanding last quarter were 962.7M, so this is a 7.8% increase in shares outstanding and it only retired $600M of the ~$1.1B of the 2026 notes. EPS, which is what most people worry about when it comes to dilution, is actually calculated based on fully diluted shares outstanding. That number actually already had a certain number of shares allocated to the 2026 notes. The fully diluted shares outstanding was 1,029.3M as of the end of Q4.

The 2026 notes were accounted for as diluted shares based on their $22.41/share conversion price. That means all $1.1B of 2026 notes were assigned ~49.6M diluted shares. Therefore, the $600M of debt that is being retired in the exchange were contributing 26.8M shares to the fully diluted share count. The exchange part of this transaction is is adding 45.9M shares to the fully diluted share count (72.6M - 26.8M = 45.9M (rounding makes it 45.9 instead of 45.8)). So there is already an extra 45.9M fully diluted shares as a result of the exchange AND they haven't even retired the entirety of the debt, just $600M of the remaining $1.1B.

Similarly, the 2029 notes also have diluted shares outstanding associated with them. It’s the 91.3M shares at the conversion price I mentioned above. So all told, the fully diluted share count should increase by 137.1M shares in Q1 as a result of these deals. That is 13% dilution. If the shares are converted as planned and dilution is not offset by gains from the capped calls, my slice of the SoFi pie would eventually decrease by around 13%. I don’t like that.

Price Action

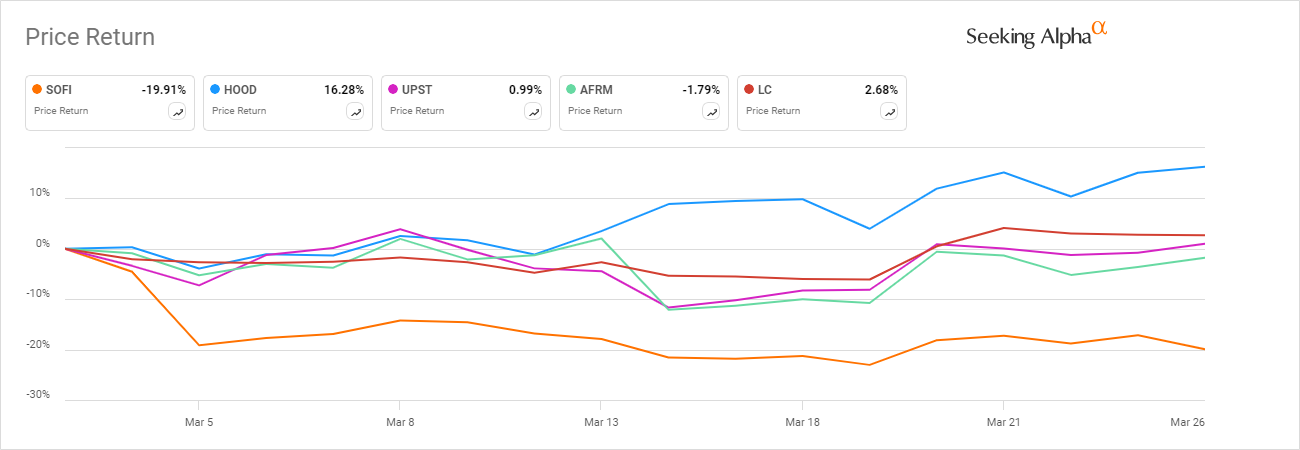

The transactions were announced in the premarket on Tuesday, March 5. I am not one who is prone to blame stock price movement on manipulation. That being said, the price action on SoFi the trading day before the offering (Monday, March 4) and especially the trading day of the announcement was extremely suspicious. SoFi has had some bad days, but the -15.3% move on March 5 was the worst day ever in the history of the stock. Through the entire 2021-2022 bear market, the $1.2B senior convertible note offering, SPAC lockup nonsense, Technisys acquisition and the dilution that came with it, the massive misses from Upstart that dragged the SoFi down in sympathy, huge CPI prints, four straight 75 bps rate hikes, a never-ending cycle of student loan moratorium extensions, a banking crisis, and more, SoFi had never had that bad of a day. The convertible note news has some negative and some positive aspects to it, but as I think will become clear, it is somewhat positive and at worst neutral on the whole.

Yet somehow that led to the largest single day drop ever. What would be the incentive to drop the stock price? Those who were buying the $862.5M in 2029 notes knew that the conversion price would be determined by the closing price at the end of that day. Every cent the stock went down is more shares for them in the future. Let's assume for a second that by 2029, SoFi manages to get back to its all time high of $25. If the conversion price were pegged to the $8.99 price where the stock closed literally two trading days earlier, the $862.5M investment would end up being worth $1.84B. However, because the conversation is calculated from a $7.27 closing price, that same investment turns into $2.28B. Convertible note holders will end up with 24% more shares than they would have gotten if the conversion price was from two days earlier. As the late Charlie Munger famously said, "Show me the incentive and I will show you the outcome."

Not only that, but as was covered above, the 2026 note holders also stood to gain more shares if the stock price stayed depressed for the three weeks after the announcement. They ended up with about the same increase in the number of shares exchanged as I just covered above for the 2029 notes. I don’t think it is a coincidence that the price action was awful for these three weeks and yet has recovered and performed better than its fintech peers since those periods ended. During the period where SoFi tanked, most fintech stocks were flat (except Robinhood, who were still flying), while SoFi was down 20%.

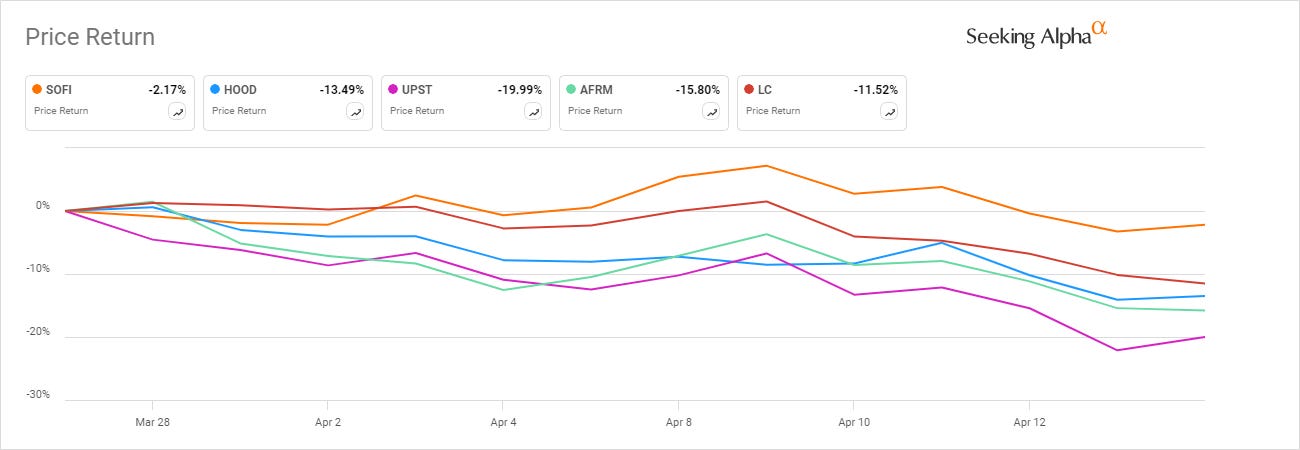

Compare that to how the stocks have performed since that window closed, where SoFi is basically flat while all the other fintechs are down double digits. Feel free to draw your own conclusions.

Positives

Interest Savings

The biggest reason to do this deal was to replace expensive debt with less expensive debt. As they stated in the original press release, the reason for the 2029 note offering was “(i) to pay fees, costs and expenses relating to this offering and related transactions, (ii) to redeem its 12.5% Series 1 Preferred Stock and (iii) for general corporate purposes, which may include repayment of higher cost indebtedness.” The preferred shares that are being a redeemed (bought back) have a 12.5% dividend. That's around $40M/yr and it was about to increase in May to over 15%, or around $50M/yr. What’s more, these had to be redeemed before May or they would renew for an additional 5 years. That is the reason that SoFi decided to put together this deal now. It costs $323.4M to redeem those shares.

Remember that they raised about $755M in cash from the deal. So what will SoFi do with the remaining ~$430M in cash? Based on what we know, and what we’ve heard from management, they will most likely use the cash to retire higher cost debt. They will opportunistically use it to retire higher cost debt that comes from the warehouse facilities or the revolving credit facility. Here, from their recent 10-K, is their highest cost remaining debt.

Let’s assume that they use all of it for the revolving credit facility. This has a sufficient amount drawn ($486M), that they could offset the majority of it. I think they’d probably pay off the portions of the warehouse facilities with higher rates first, so saying they are using it all for the revolving credit facility should give a low estimate of how much interest they’ll save. They are effectively refinancing $430M at a 6.95% interest rate with 1.25% debt. That works out to an additional $24.5M in annual interest savings. Add that to the $40M saved from retiring the preferred shares, and you end up with about $65M in annual interest savings that should go straight to the bottom line. That is great for the profitability of the business moving forward.

Large Capital Raise

One of the biggest recent SoFi bear cases was that their capital ratios were getting tight and any large downturn in the economy could lead to high defaults and put them at risk of regulators stepping into to force them to liquidate their assets. That bear case is now effectively dead. I covered all the background info on capital ratios and how it affects how much SoFi are able to lend in this post if you want to read up on it.

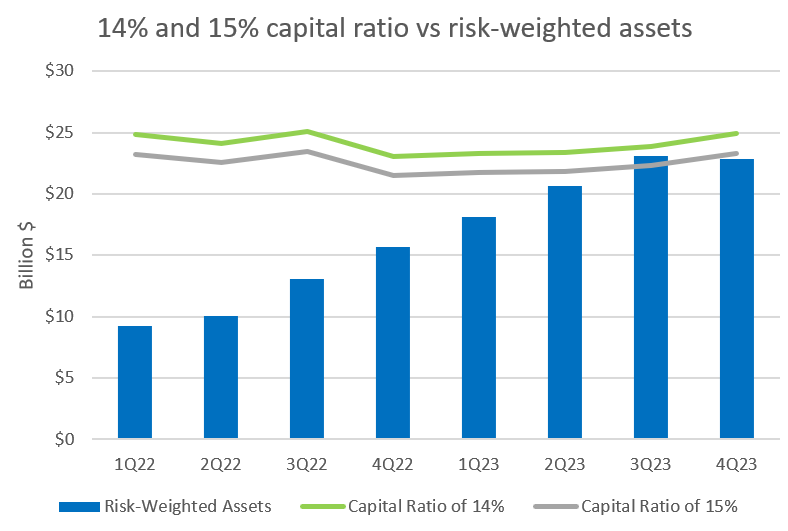

SoFi was close to the limit of where they could keep growing their balance sheet. Much of their recent growth came from their ability to originate loans, hold them, and make more interest income from holding more loans. Some additional growth came from the noninterest income generated by originating loans and marking them at fair value. From Q3 to Q4, for the first time since becoming a chartered bank, their total risk-weighted assets (a fancy way to measure how many loans they are holding) decreased. That essentially means that the amount of loans paid off, charged off, or sold in Q4 was greater than the amount originated. It was anticipated that the amount of risk-weighted assets balance sheet would remain close to flat throughout 2024.

In the Q4 2023 earnings call, they said to expect “to end the year with a total capital ratio north of 14%”. They were at 15.3% last quarter and intend to grow tangible book value by $300M-$500M this year (which translates roughly to about the same growth in their total risk-based capital). This transaction adds about $500M in total risk-based capital for the company (the $600M in retired debt less the $17M in fees and ~$90M they paid for capped calls). $500M in capital translates to about $3.5B in assets they can add if you assume a capital ratio between 14%-15%.

I think this is easier to understand visually. The graph below shows SoFi’s quarterly risk-weighted assets along with two lines that represent where the assets would be at a 14% and 15% capital ratio. You can see that since getting the bank charter they rapidly built the balance sheet until Q3 2023.

The bear case was that if SoFi can’t grow the balance sheet, that means they can’t grow lending revenue, and that they can’t withstand losses without regulators stepping in. While I disagree with some of those arguments (especially the one about losses), the extra capital from these transactions thoroughly derisks SoFi from a balance sheet perspective. Below you can see the continuation of the capital ratio of 14% and 15% if there were no transaction compared to what they will be in actuality because of the transaction. This assumes $400M in tangible book value growth (the midpoint of their guidance) with and without the transaction. The green and gray bars are my estimate of what will actually occur. The red and yellow bars are what would have happened if there were no transaction. It’s obvious that the extra capital raised through these transactions has a huge effect on how many assets (loans) they can hold to maintain a capital ratio “north of 14%”.

That graph, in my estimation, is the main reason SoFi chose to retire the $600M in 2026 convertible notes with shares rather than cash. Had they done it with cash there would have been almost no benefit to the capital ratios. The ~$70M in gains they got from buying the 2026 notes back at 89 cents on the dollar would have been completely offset by the fees and cost of the capped calls associated with the 2029 notes offering. The flexibility they get for the balance sheet moving forward was paid for by dilution. How they use that flexibility moving forward will determine if that dilution was worth it.

Earnings and Tangible Book Value per Share

SoFi gets to count the difference between the $529.5M they are paying with shares and the $600M of debt they are retiring as a profit. Additionally, moving forward they are now saving a lot of interest expense in perpetuity as a result of the transactions. This is why Anthony Noto in his interview with Jim Cramer, said that the transactions as a whole are neutral on an EPS basis.

We already covered that tangible book value will increase by about $500M as a result of the transactions. Their TBV was $3.3B last quarter, so it will increase by about 15% as a result of the transactions. Fully diluted share count increases by about 13%. So this transaction does improve their TBV/share. Many (not including me) think that banks should be valued on their TBV/share, so those people ought to be pleased by this set of transactions.

Guidance

I had the opportunity to talk with SoFi Investor Relations and clarify what was and was not included in the guidance from this transaction. Obviously they had some idea that this deal was going to go through this quarter, and portions of the deal were included in their full year guidance. After it was announced it made portions of their guidance much more clear than they were before, especially concerning GAAP net income and EPS.

SoFi knew they’d be paying off the preferred shares during Q1 and they did include the redemption of those shares in the guidance. Before, it made little sense that SoFi’s GAAP net income guide was $95M-$105M while its EPS guide was $0.07-$0.08. SoFi calculates GAAP net income before accounting for the dividend for the preferred shares, whereas EPS is calculated after subtracting that dividend out. Those dividends would have been around $45M this year. They have >1B fully diluted shares outstanding, so $95M-$105M in GAAP net income should have corresponded to $0.05-$0.06 in EPS. Now that they’ve only paid about $10M in interest in Q1 and won’t have that dividend to pay in future quarters, and their fully diluted share count is slightly higher, the guidance for GAAP net income and EPS match.

Investor relations also clarified that the equity issuance was not incorporated into their guidance. In other words, the possibility to step on the gas in lending and expand the balance sheet was NOT included in the guide. I asked specifically if the extra buffer in capital ratios would mean they would lean into greater lending growth relative to their guidance. They reiterated that they expect to be conservative as Chris Lapointe talked about at the UBS Conference. Here is how he described their view on the macro and originations at the end of February before the deal was announced (I have lightly edited this quote to make it read better):

Looking forward, I think an awful lot would have to change for us to take a different stance on originations over the course of the next 12 months. There's still a ton of volatility with respect to rates. If rates do come down 4, 5, 6 times as expected, what does that actually mean and imply? Yes, it may be great for a refi business, but does that necessarily mean that the economy is doing well and we should accelerate lending? We would have to evaluate at that given point in time, given all the factors that are at play. Right now, a lot would have to change and a lot more certainty with respect to the macro would have to change for us to get comfortable. The only other thing I would say there is like we are able to operate very nimbly and allocate capital as necessary to maximize shareholder value and return on those invested dollars.

Management has historically been quantitatively conservative with their forward metrics but qualitatively clear and direct about the business. I still fully expect that they will be conservative not only in their guidance but also in their lending execution until they see a clearer macro picture. However, the capital raise gives them the ability to lean into lending growth as the macro picture clears up. This will give them additional upside at that point.

I do not know whether the picture will become clearer in the back half of this year or further into the future. What they did say to me is that the extra capital gives them “further runway for incremental growth when we have more clarity on the broader macro and feel more comfortable with investing more in driving growth.” My interpretation is that the buffer they just got in their capital ratios will be utilized, but not until they feel more confident in the economy and future rate movements as Chris Lapointe described.

My Take

I love the 2029 convertible note deal. Redeeming the preferred shares is a slam dunk. The interest on the entire $862.5M in notes will cost less than what they were due to pay on the $323M of preferred shares. The other debt they are replacing is similarly at a much higher interest rate and they will save a lot of interest expense. That was great business.

I don't like that they are diluting at such a low stock price because I think SoFi is very undervalued at these prices. Let's assume for a minute that by the end of this year the stock price gets to $15 and they can buy back the $600M with no discount ($1 for $1). That would only be 40M shares, not 72.6M shares. They could dilute for less if they waited for a higher stock price, but then would not have gotten the same gain in total capital nor the GAAP net income boost from paying the debt off at a discount. The original terms for the entire $1.1B in 2026 convertible notes at their redemption price would have resulted in at most 49.6M in dilution. What actually happened is more dilution than originally planned, and does not extinguish all the debt. On the face of it, I do not like that at all.

I wish they would have gotten a better price. The 2026 convertible notes had an effective interest rate of 0.43% interest and didn't convert unless the stock price was at $22.41 by October 2026. That's a crazy low rate they could have taken advantage of for the next 2.5 years and the conversion price is way higher than the current stock price. It seems like they could have negotiated a steeper discount than 89 cents on the dollar to trade in no-cost debt in the current environment. A steeper discount would have meant more tangible book value growth and less dilution.

I also don't know how independent these deals were. If they could have just done the 2029 convertible notes and not the dilution and buyback of $600M, that might have been a better path. My suspicion is that the deals were linked, although that is also speculation. If so, the extra dilution that they had to give up in order to avoid 5 years of interest payments on the preferred shares seems like it was probably worth it. That’s about $250M in interest they saved by doing the deal now, not including other interest savings.

Conclusion

If you look at the deal in its entirety, there is lot to like. It is still a mixed bag, but on the whole, this deal is a net positive with one caveat. That caveat is that they have to execute as well moving forward as they have in the past. The extra capital really gives them leverage to grow earnings at a compounded rate faster than the rate of dilution. I trust them to execute, and I trust that they have the best interests of the company and shareholders in mind. Here is a quick summary of the good and the bad from the deal.

Positives

Saving somewhere around $60M-$75M in annual interest ($40-50M from the preferred shares and $25M from other higher interest debt)

Increases tangible book value and total risk-based capital by about $500M

Quells fears about balance sheet

Accretive to TBV/share and neutral on EPS

Gives them room to grow lending again when the macro picture clears up

Negatives

Fully diluted share count is increasing by about 13%

Shares outstanding are increasing by 7% in Q1 as a result of the 2026 note exchange

Stock price was crushed as a result of the news

Management have a significant portion of their own net worth tied to the performance of the company and the stock. There is a lot of shareholder alignment in their compensation packages. In fact, moving forward with their new compensation package, a greater percentage of their future stock-based compensation will be tied to performance rather than just given automatically. I trust the SoFi team to put their heads down and operate the business in a way that makes this deal worth it. If they continue on the path they've been on for the last 3+ years, I'm still very confident that I'll be a well-rewarded investor in the long run.

Subscriber update

I am basically treading water right now with paid subscribers. My goal before starting a YouTube channel is to get to 100 paid subscribers.

Right now I am comfortable with taking the time to write about 2 articles every month. Once I get to 100 paid subscribers, I’ll start a YouTube channel and do at least one video every other week (I plan on also posting those on X).

Paid subscribers also get access to a private X chat. If you are a paid subscriber and not in the chat, please email me at datadinvesting@gmail.com and let me know and I’ll get you added. If you have any other ideas for things I can do to bring value to my paid subscribers, don’t hesitate to reach out.

Disclosures: I have long positions in SoFi.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Does anyone know why they have to have a cap for the capped call? Why not just do a call option by itself with higher upside?

Finally got around to reading the whole thing. Your work is of great service. Thanks as always Chris.