SoFi: The Moat is Being Built - Part 1

A common refrain I still hear from people who do not think SoFi is a good investment is that there is significant competition and that SoFi does not have a moat. This means there are low barriers to competition and anybody can just copy the business. Let’s discuss moats in general before moving on to discuss SoFi’s moat specifically.

Moats Are Built, Not Bestowed

In 1995, Warren Buffett said,

“The most important thing [is] trying to find a business with a wide and long-lasting moat around it … protecting a terrific economic castle with an honest lord in charge of the castle.”

The most successful companies have something unique that distinguishes them and makes them unrivaled in some way. Moats can take the form of brand, technology, patents, high barriers to entry, cost savings, network effects, or numerous other competitive advantages.

Apple has their brand and ecosystem. Google is far and away the most used search engine. Amazon is the first place you look to buy pretty much anything. Here is the thing though, it isn't like some magical moat fairy came down, waved her magic wand, and granted these tech giants an unassailable position at the top of market cap mountain.

I'm old enough that I remember opening up multiple instances of Netscape Navigator to type the same search query into Lycos, Google, Excite, Infoseek, Yahoo, and (my personal favorite at the time) AltaVista to see which search engine turned up what I was looking for. I remember when Blackberry was the market leader in smartphones, and I remember buying books from Amazon when that was all they sold.

Google dug their moat by engineering a superior algorithm and caching results for commonly searched words and phrases. They became the de facto search engine because their results were consistently the most relevant and their response time was faster. At the turn of the millennium, 17% of web users visited AltaVista at least once a week and only 7% of web users visited Google once a week. Sometime around 2004, Google’s market share went above 50% and it only grew from there. They widened that moat by staying nimble and giving free or low-cost access to an ever-growing suite of products (Gmail, Drive, Photos, etc.) and making the greatest acquisition of all time (YouTube).

Apple went from failing at their current business to becoming the most valuable company in the world in less than a decade. Seriously, from the mid-90s to mid-2000s, their main revenue generator was computers, their niche market were designers, and they were getting crushed. Windows 95 cut their already single-digit market share in half and it stayed that low for a decade, hovering between 2-3%. Then the iPhone happened, they built an ecosystem that has unrivaled interoperability, and now they are the most valuable public company that has ever existed.

The point is that, with the rare exception of heavy patent protection, a moat takes time to dig and fill with water. As good companies grow, they make it deeper, wider, and fill it with sharks with laser beams attached to their heads. Anyone could have reasonably argued that Google was "just a search engine," Amazon was "just a retailer," and Apple was "just a failing computer manufacturer." Moats are the result of creative vision, leveraging competitive advantages, and exceptional execution. A moat is built, not bestowed. What determines whether SoFi will be “just a bank” or the “winner take most in the fintech space” is their execution.

SoFi's consumer business

SoFi's pitch is pretty simple, it's a "One-stop shop for all your financial needs." The products include checking and savings accounts, investment and crypto brokerage (including IRAs and robo-advisors), credit card, personal loans, student loans, mortgages, SoFi Relay (finance tracker, budgeting, and credit score tracking), insurance offerings, and other smaller products. They want to be there for and support their members (what they call their customers) through every part of their financial journey. The playbook they have is laid out by CFO Chris Lapointe (I've lightly edited his words for brevity and clarity):

We have deployed a strategy that we call the Financial Services Productivity Loop, and that has three main components."

The first one is creating a comprehensive set of products that are each and individually best-of-breed [...] in addition to that, we want each of those products to work better when they're used together."

The second key element of our overall strategy is to have superior unit economics across each and every one of our products and vertical integration is a key component of that."

The third component is investing in our fintech platform in pursuit of becoming the AWS of fintech."

We won’t talk about the AWS of fintech in this article, but I have covered it before for anyone who is interested.

The data give insights into the moat

So why did I decide to write an article about SoFi’s moat now? CEO Anthony Noto is fond of saying that when he joined in 2018 that everyone was talking about being an all-in-one financial app, but that SoFi is the only company who has actually done it. However, SoFi’s moat has been mostly theoretical. They say a one-stop shop should allow for a better experience and cross selling. They argue that it will increase user engagement and drive greater lifetime value from their members. Essentially, it should make SoFi’s results differentiated from their competitors. That should be noticeable in the results. The data is showing that the moat really is forming.

Deposits

SoFi has a focus on getting new members to move their direct deposit to SoFi. That is because the bank where you send your direct deposit is almost always your primary bank, and your primary bank is where you keep most of your money. Here is what was said on the earnings call about deposit growth:

From a balance sheet perspective, our unique value proposition in SoFi continues to fuel high-quality deposits, that increased by $2.7 billion sequentially and we ended the quarter with nearly $12.7 billion in deposits. Importantly, more than 90% of our consumer deposits are from sticky direct deposit members, and nearly 98% of our deposits are insured.

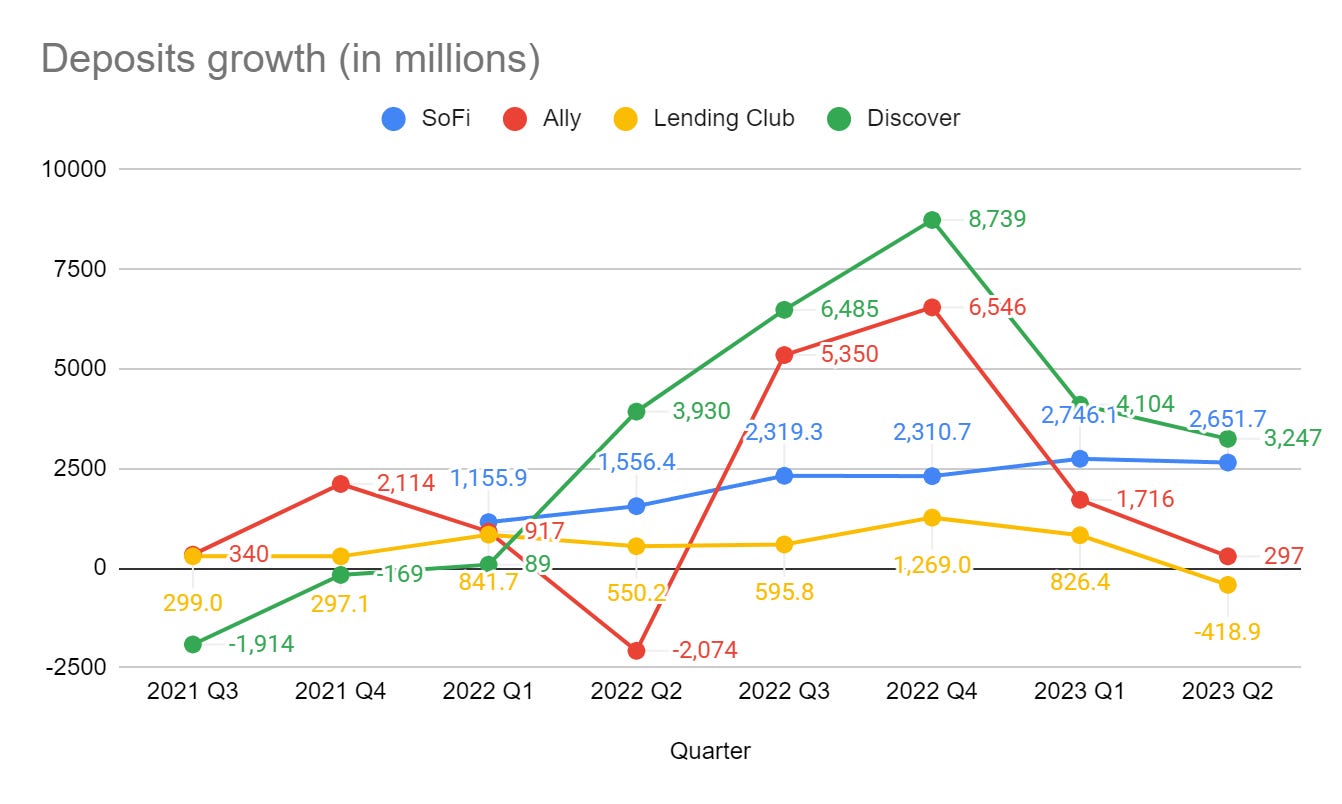

Big deal, SoFi is getting a lot of deposits because it’s offering a high APY (4.5% at the time of writing), right? Ally currently gives 4.25%, LendingClub clocks in at 4.5%, Discover is at 4.3%. LendingClub had higher APY than SoFi for the entirety of 2Q23. If it all came down to APY, they should have also seen significant deposit growth, as should the other digital neobanks. Credit to Vadim Kotlarov for this graphic, you should follow him on twitter @VadimKotlarov and subscribe to his substack.

Every neobank has seen deposit growth over the past year as they’ve been taking customers away from incumbent banks by offering higher APYs than the likes of J.P. Morgan, Wells Fargo, and Citi. However, peak deposit growth for neobanks was 4Q22 and they’ve all seen a steep drop off in deposit growth thereafter. Only one company has bucked this trend, with SoFi’s deposit growth continuing to accelerate. LendingClub even saw deposits shrink in the quarter despite offering higher rates that SoFi the entire quarter.

When you see a definitive trend reversal like that across an entire industry with one outlier who bucks that trend, you should take note. Especially when on the face of it there is no reason for them to buck this trend. It isn’t like SoFi gave higher APY or even higher signup bonuses during these last two quarters as they were before. This is a testament to the fact that their product is differentiating itself in other, less obvious ways. This is what a moat looks like.

Customer Acquisition Cost

I covered this in my last article, but it is also applicable here. SoFi is paying less in customer acquisition costs (CAC) than they have in well over a year and adding more members than they ever have before. The title of the article was taken from CEO Anthony Noto’s quote from the earnings call, here is the full quote:

And I think this quarter is the first quarter that I can say, I feel really confident the flywheel is really working. And what I mean by that is, we're seeing efficiencies in our customer acquisition cost. And those efficiencies are really more correlated with the unaided brand awareness being increased in addition to the fact that our marketing and product teams are iterating every day through technology and content information analytics to drive those efficiencies. […] It's the holistic approach that we've taken over the last 5.5 years that is really starting to pay off in the quarter and as we look into Q3 as well.

I love that he said that this trend is continuing into Q3 as well. One quarter of lower CAC and high member adds is not definitive proof that they truly have turned a corner. However, the increase in brand awareness also provides data that supports this trend. If CAC can stay low as quarterly new members climb, it would be another piece of evidence that the moat is growing.

The Moat is Growing

I think its very derivative to say a company either has a moat or doesn’t have a moat. All companies have some sort of a moat. Some of them are wide and deep, others are narrow and shallow. For younger growth companies, I think it is very important to look at the rate of change of the moat rather in addition its absolute size.

Is there competition in the personal finance space? Absolutely there is, and there is a lot of it. However, if the data say that a company is taking market share and posting differentiated results, it’s indicative of a widening moat. SoFi is the best all-in-one digital banking app of which I am aware. The data are suggesting that SoFi’s products are differentiated and their moat is growing. The lending data are even more clear in this regard, but that’s a topic for the next article…

Thanks for reading everyone. Please make sure to become a free subscriber by entering your email, or a paid subscriber if you feel you’ve gained value from my work. Always 100% voluntary.

Disclosures: I have long positions in SOFI, GOOGL, and AMZN.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

Part 1 means there will be 2 and 3 probably? I am excited!