How Risky is SoFi's Loan Portfolio?

Spoiler alert: Not as risky as many think

Delinquency and default risk to revenue and profits

I’m going to start by laying out the risks associated with SoFi’s loan portfolio. Almost all the loans on SoFi’s balance sheet are unsecured personal or student loans. This makes people really nervous because there is no financial backstop if the borrower stops paying a personal loan. A secured loan, like a mortgage or auto loan, uses a tangible asset as collateral that at least keeps the lender from huge losses. If someone defaults on their mortgage, the bank can foreclose on the house, if they default on their auto loan, the bank can repossess the car. The bank might lose some money on the transaction, but they at least have a car or house to sell to cover part of those losses.

If someone with a $10,000 SoFi personal loan goes into default, SoFi can send it to collections and hope to get some money back, but they have to eat the entirety of that $10,000 loss. This is why personal loans are considered much riskier than secured loans. However, banks compensate for the elevated risk by charging a much higher interest rate on personal loans than they do on secured loans. That means that as long as the borrower repays the debt, personal loans are way more profitable than mortgages or auto loans. The chart below puts into context just how much SoFi has grown their loan book and how it has shifted to being weighted more toward personal loans.

We know that when people lose their jobs and the economy goes into recession, more people default on their loans. That default causes a direct hit to revenue because it gets accounted for as a hit to noninterest income. This, to me, is by far the most important risk because SoFi is a growth story. If we hit a deep recession and defaults really spike, it will ruin the trajectory of SoFi’s finances. Revenue growth caves, profitability gets pushed out further into the future, and SoFi’s lending segment, which is its cash cow, stops churning out cash to cover for R&D spend for Galileo and to cover the currently unprofitable financial services segment. SoFi has to engage in cost cutting measures to right the ship and it hurts their ability to continue to scale their business and invest in new revenue streams. That is a risk.

It’s also helpful to define the difference between delinquency and default up front. A delinquent loan is one that has payments that are past due. SoFi tracks these and marks them down. SoFi marks the loans down at 10 days past due, 30 days past due, and 90 days past due. At 30 days delinquent, they’ve already written off 70% of the value of the loan, and at 90 days, they account for them as only worth 10% of the remaining prinicipal. Those write-downs immediately hurt SoFi’s revenue during the quarter when they happen. Default on their loans occurs when they are 120 days past due. The loans are charged off completely (meaning they are worth nothing to SoFi anymore) and handed over to collections.

The end of days liquidity scenario

This is the bankruptcy scenario. If we get into a deep recession and defaults really spike, SoFi has to cover that loss with their own cash. The mounting losses lead to fear, which leads to a bank run, and SoFi does not have the liquidity to cover their deposits. The FDIC steps in and SoFi stock goes to 0.

How risky are SoFi’s loans?

Here is where the risk narrative, for me at least, breaks down. SoFi manages delinquency risk by maintaining extremely high credit standards. Their personal loan borrowers have a weighted average income of $164,000 and a weighted average FICO of 747. They have a hard cut off at a FICO score of 680, below which they will not lend at all. This puts them well above peer lenders such as Upstart, who cater to subprime and near prime borrowers, and LendingClub, who lend primarily to prime and prime plus borrowers. SoFi has exposure to increased delinquencies and defaults, but the quality of their borrower should keep them insulated unless we see a very deep recession.

Additionally, SoFi originates to free cash flow, meaning that the key consideration for them is not a backward-looking analysis of how well you’ve paid off your debts in the past. That’s just the first hurdle that borrowers have to get over. The key consideration for them is how much extra cash flow borrowers have to pay the loan. This is a forward-looking metric to gauge how likely they are to default in the future. Obviously if people lose their income then defaults will rise as their cash flow hits a wall. That is a risk, but I’ll discuss this more below.

Finally, many are suggesting that SoFi’s default rates will rise once student loans come back as many of their borrowers also hold student loans. Two points on this. First, if borrowers already hold SoFi-refinanced student loans, they’ve already been paying those bills. Seond, SoFi accounts for that in their free cash flow calculations. CEO Anthony Noto was asked about this on June 7 at the Piper Sandler conference, “Do you anticipate that there will be an increase in defaults on other products just because of the student loans or do you feel like that's handled with the underwriting you already put in place?” Here was his response:

It shouldn't have an impact on our personal loan performance, because when we underwrite a personal loan, we're forecasting that applicant’s and that future member’s ability to pay based on their cash flow and we're asking them for a bunch of data that allows us to determine what their cash flow is.

In addition to that, we do a credit pull. So we see all their liabilities. And if they had an existing student loan, even if they weren't paying it, it would have shown up on the liability side and that would have been assumed as a necessary payment within that cash flow. So it should have no impact. The student loan was part of that overall decision criteria in the personal, as well as all the other debt at that moment of financing. So it should have no direct impact, everything else being equal.

Now, I wouldn’t go so far as to say that it should have no impact as he stated. An additional bill each month will put extra strain on borrowers, and it may result in an uptick in defaults. However, it is important to recognize that SoFi has already done their best to account for this in their underwriting, so it should not have an outsized effect on their loans.

Historical Data

How much does high-quality borrowers insulate SoFi from defaults in times of financial stress? Fortunately, there is data for that. Transunion, one of the premier credit reporting agencies, wrote an analysis on personal loan and credit card delinquencies during the Great Financial Crisis (the original URL now forwards to a newer article that covers something completely different, so I’ve included a link to the original article through the wayback machine). They looked at the FICO scores of borrowers in 3Q 2007 who held personal loans at that time and tracked their delinquency rates over the next three years. The table below shows their findings:

This data includes all loans that had been originated and were still to be paid off, so it also includes seasoned loans with vintages prior to 2007. However, the data clearly show that FICO score provides a significant margin of safety to lenders. SoFi's borrowers fit squarely in the Prime Plus category, which showed a cumulative default rate from 2007 until 2010 of less than 1%. I understand those who worry about defaults if we are entering a recession, but I find it very unlikely that the credit crunch and recession that is coming will be worse than the GFC. I could be wrong about that.

SoFi-specific data

Not only are SoFi’s borrowers historically in a range where defaults will remain low, but SoFi is seeing industry-leading default rates right now in the current environment. Upstart publishes their Upstart Macro Index every month, which “estimates the impact of the macroeconomy on credit losses for Upstart-powered unsecured personal loans”. In other words, if default rates are at normal rates, UMI is 1. If loans are overperforming because of the macro environment (like because the government gave out a bunch of stimulus checks), UMI is less than 1. If loans are underperforming (like when stimulus checks run out and inflation is at 40 year highs), the UMI is above 1. Here is the current UMI:

Upstart’s loans are currently defaulting at a rate that is 1.5x normal performance. How about LendingClub? They used to highlight that their delinquencies were still performing better than their prepandemic levels. That commentary ended in 3Q22. In 4Q22, this is the slide they showed:

Notice that delinquencies had risen back to prepandemic levels again. This slide was conspicuously absent from the 1Q23 slide deck. Let’s compare that with SoFi management comments from their 1Q23 earnings call:

In other words, SoFi’s risk models and delinquencies are well below their competitors. If a recession comes, that trend will almost certainly continue to hold true. SoFi’s underwriting is objectively better than their competitors.

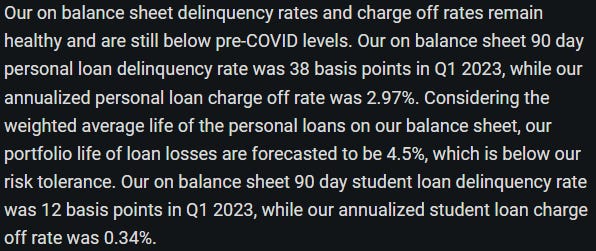

Delinquencies and Defaults are Increasing

I like to highlight the bad as well as the good. The truth is that since their loan portfolio is still relatively young, and since we are entering a period of turmoil in the economy, both delinquencies and defaults are absolutely on the rise for SoFi. The stimulus money that caused loans to overperform has dried up and we are returning to normalcy. SoFi’s management has forecasted this, and it is not surprising, but this is something to keep an eye on. Delinquency rate should lead charge-off rate, so I will be keeping a close eye on delinquencies moving forward. Notice that there are two y-axes on this graph. Also note that delinquencies are reported at where they stand at the end of the quarter. The charge-off rates are annualized.

I expect this to continue to rise over the next few quarters, and that SoFi, like LendingClub and Upstart, will get to the point where they can no longer make the claim that they are below prepandemic levels for charge-offs and delinquencies. However, the fact that it is taking longer for them to get above those levels still shows better underwriting than competitors.

Guidance

SoFi’s guidance takes three things into account that are now much less likely to happen. First, the guidance assumed that the fed funds rate would peak where it is and that there would be two rate cuts in the back half of the year. Second, SoFi assumed a 5% unemployment rate exiting the year. Last, they assumed a 2.5% contraction in GDP. It certainly looks right now that there will not be two rate cuts. That isn’t great for SoFi, but they have hedges in place against rate movements. Higher rates are bad for student loan refinancing, but even at current rates or slightly higher rates, there is still a lot of incentive to refinance for other reasons. Credit card rates staying high should provide continued robust demand for their personal loan business. Higher rates probably hurt them overall, but only marginally.

However, something most people glossed over from the FOMC meeting this week is that the Fed is projecting lower unemployment and higher GDP growth than they did in March. Here are their projections:

The median projection of the Federal Reserve Board members is for unemployment to be at 4.1% and GDP to grow at 1%. Rates staying higher for longer is a bit of a headwind for SoFi, but if unemployment ends the year almost a full percentage point below SoFi’s projections, that’s a really big tailwind for the business. If the economy keeps up even 1% real GDP growth, that also signals way more upside for SoFi than their guidance, which assumes a 2.5% contraction. Delinquencies and defaults are going to be tied primarily to unemployment. This leaves a lot of room for SoFi to outperform their guidance and raise future guidance because their assumed loss rates appear to be much worse than what will actually play out.

The Bottom Line

SoFi is not at some existential risk of going under. Most people who worry about their loan book are uninformed and are making ad hoc arguments but haven’t looked at the underlying data. Opinions are noise and data is evidence. The data show that SoFi has high quality borrowers who perform significantly better in adverse economical conditions. The data show that SoFi’s underwriting is outperforming all of their chief competitors. The data show that SoFi’s guidance has baked in more losses on their loan portfolio than is likely to actually occur. This suggests that the most likely outcome is that SoFi will outperform their own guidance and therefore Wall Street’s guidance, since they are very similar.

Make no mistake, if we see a deep recession, mounting losses could derail SoFi's growth story and profitability projections. There are scenarios where the growth grinds to a halt and SoFi is stuck treading water until the economy recovers. However, I see almost no realistic scenarios where the end of days liquidity scenario above is even remotely possible. If SoFi is forced to hold their loans to maturity, they are good enough loans that they’ll still make great money on them. It just means they can’t accelerate using a capital-light approach of selling loans and originating new ones to continually refresh the balance sheet. I think that in most realistic scenarios, SoFi’s loans will outperform their targeted and guided loss rates, results will be better than expected, and the growth story will continue on a trajectory faster than analyst expectations.

Please make sure to become a free subscriber by entering your email, or a paid subscriber if you feel so inclined. Always 100% voluntary. Thanks for reading everyone.

The information contained in this article is for informational purposes only. You should not construe any such information as legal, tax, investment, financial, or other advice. None of the information in this article constitutes a solicitation, recommendation, endorsement, or offer by the author, its affiliates or any related third party provider to buy or sell any securities or other financial instruments in any jurisdiction in which such solicitation, recommendation, endorsement, or offer would be unlawful under the securities laws of such jurisdiction.

From what I've been hearing, we're going to see more interest rate increases, and no cuts this year 2023. They didn't raise in June, purportedly to wait for more data. Australia, Canada, and European communities are still raising rates. I hope they make more progress slowing inflation, because many things seem very expensive.